For over a decade, Cyprus has promised to fix its title deed crisis. Thousands of property buyers — many of them foreign nationals — purchased homes and apartments only to discover that legal ownership documentation was never transferred. Developers carried unpaid bank mortgages on the land. Banks refused to discharge liens even after receiving full payment. And the government looked the other way. On February 13, 2026, the Department of Lands and Surveys finally activated the administrative fines procedure under Law 81(I)/2011, turning a paper-tiger statute into an operational enforcement tool with real financial teeth.

What Changed: From Dormant Law to Active Enforcement

The Sale of Immovable Property (Specific Performance) Law No. 81(I)/2011 was designed to protect property buyers by ensuring enforceable contracts and timely title transfers. For fifteen years, the law existed on the books but lacked a functioning penalty mechanism. The February 2026 activation, formalized through amendments under Law 132(I)/2023, introduced a graduated fine structure that targets the two primary bottlenecks in the title transfer process.

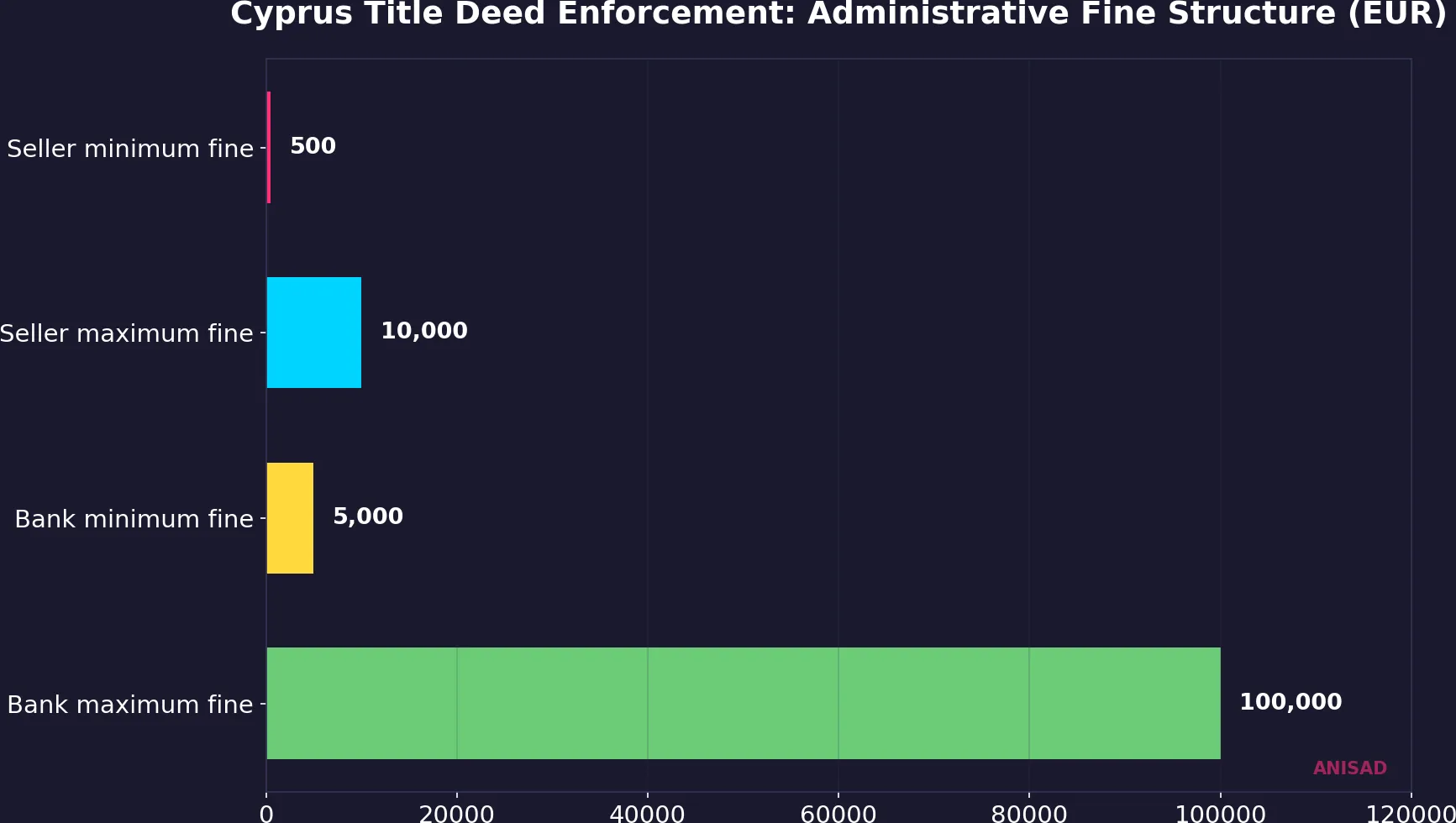

Sellers are now required to attach a Search Certificate dated within five working days of contract conclusion. Failure to comply triggers fines ranging from EUR 500 to EUR 10,000, scaled to the purchase price. Mortgagee banks that fail to discharge or release mortgages after receiving full buyer payment face significantly steeper penalties: EUR 5,000 to EUR 100,000 per violation. A three-month transitional period runs until May 16, 2026, after which full enforcement begins.

The Scale of the Problem

The title deed crisis is not a minor regulatory inconvenience — it is a structural defect that has undermined confidence in Cypriot real estate for more than a decade. An estimated 10,000 or more property transactions remain unresolved, with buyers who paid in full still lacking legal ownership documentation. This backlog is concentrated among developments completed between 2005 and 2015, particularly in Paphos, Limassol, and Larnaca, where speculative construction financed by overleveraged developers left a trail of encumbered titles.

The root mechanism is straightforward but pernicious: a developer takes a bank loan to build a project, sells units to individual buyers, but the original mortgage on the land is never discharged. The buyer has a contract and possession, but no title deed. The bank holds a lien that supersedes the buyer's claim. Until now, neither the developer nor the bank faced meaningful penalties for maintaining this status quo.

Fine Structure: Who Pays What

The fine structure is deliberately asymmetric. Seller fines are calibrated to the purchase price, with a maximum of EUR 10,000 — meaningful for individual transactions but unlikely to threaten business viability. Bank fines, however, reach EUR 100,000 per violation — a level designed to make systemic non-compliance economically unsustainable. For a bank processing hundreds of mortgage discharges annually, even a small compliance failure rate would generate substantial cumulative penalties.

Who Benefits and Who Faces Risk

The enforcement regime creates a clear set of winners and losers across the Cyprus property ecosystem.

Property buyers — particularly foreign purchasers who have historically been most vulnerable to title deed delays — gain the strongest protections. The graduated penalty structure gives the DLS a practical tool to compel compliance, rather than relying on voluntary cooperation from developers and banks. For buyers with pending title transfers, the transitional period ending May 16 creates an implicit deadline: any obstruction beyond that date carries immediate financial consequences for the obstructing party.

Responsible developers with clean title transfer records gain a competitive advantage. In a market where foreign buyer due diligence is intensifying, the ability to demonstrate a track record of timely title transfers becomes a selling point. Conversely, developers carrying large backlogs of unresolved titles face both direct financial penalties and reputational risk. Some of these developers may discover that their balance sheets cannot absorb the cost of compliance — particularly if outstanding mortgages need to be restructured to enable discharge.

Banks face the most significant financial exposure. The EUR 100,000 maximum fine for mortgage discharge failures is designed to make non-compliance more expensive than compliance. This is a deliberate calibration: for years, banks had no economic incentive to process mortgage discharges promptly, since the administrative cost of doing so exceeded the penalty for delay (which was effectively zero). The new fine structure inverts this equation.

Market Implications: Liquidity, Confidence, and Institutional Capital

The activation of title deed enforcement carries implications well beyond individual buyer protection. Cyprus's property market has seen sustained price growth, with the CYSTAT House Price Index reaching 152.93 (base 2015=100) in recent quarters, representing a 4.2% year-over-year increase. This growth has occurred despite the unresolved title deed overhang — a remarkable demonstration of demand resilience, but also a vulnerability.

Secondary market liquidity should improve materially as clean-title properties become more tradeable. Properties with unresolved title issues trade at a discount or are effectively untradeable, locking both buyers and capital into illiquid positions. Resolution of these cases would unlock significant dormant value and increase transaction volumes in the resale market.

Foreign buyer confidence is the critical variable. Cyprus competes with Greece, Spain, Portugal, and Turkey for international property investment. Title deed risk has been a persistent friction point in due diligence processes, particularly for institutional and diaspora buyers. If enforcement proves effective, expect increased foreign transaction volumes within 12 to 18 months — particularly from buyers who previously avoided Cyprus specifically because of title risk.

Institutional capital requires clear legal title as a non-negotiable prerequisite. The title deed crisis has been a direct barrier to institutional real estate investment in Cyprus. Resolution of the backlog would position the market more favorably for institutional entry, potentially accelerating the professionalization of the sector.

Hidden Risks: Developer Balance Sheet Exposure

Active enforcement could surface hidden liabilities on developer balance sheets. Some developers who used buyer deposits to finance other projects — rather than to discharge project-level debt — face a double bind: they must now either restructure outstanding mortgages (requiring fresh capital or bank negotiations) or face escalating fines. For overleveraged developers, this creates genuine solvency risk.

The banking sector faces its own adjustment costs. Processing thousands of mortgage discharges simultaneously will strain compliance departments and require system-level changes to workflows. Banks that delayed discharge as a passive revenue strategy (continuing to collect interest on undischarged mortgages) will need to absorb the income reduction alongside the compliance costs.

What to Watch

The May 16, 2026 deadline — when the transitional period ends — is the first critical milestone. The market will judge this reform not by its language but by its implementation. Key signals to monitor over the next 6 to 18 months include:

- Volume of title deed transfers processed in Q3-Q4 2026 compared to historical averages

- Number of administrative fines actually levied by the DLS after May 16

- Bank mortgage discharge processing times — any systemic acceleration would confirm behavioral change

- Foreign buyer transaction volumes — a lagging indicator, but the ultimate test of restored confidence

- Developer financial disclosures — watch for restructuring announcements or project-level impairments

Conclusion

Cyprus has had a title deed enforcement law since 2011. It has taken fifteen years to activate the penalties. The question now is not whether the legal framework is adequate — it is whether the institutional will exists to apply it consistently. If the DLS enforces the graduated fines as written, the title deed backlog should begin clearing within 12 to 18 months, fundamentally improving market integrity for the first time in a generation. If enforcement proves selective or toothless, the reform will join a long list of regulatory promises that failed to change the underlying dynamics. The stakes are not abstract: thousands of property owners are waiting for the answer.

Data sources: Cyprus Department of Lands and Surveys (DLS) official portal, Sale of Immovable Property (Specific Performance) Law No. 81(I)/2011, Law 132(I)/2023 (amendments activating administrative fines), CYSTAT House Price Index (base 2015=100)