Cyprus is approaching a regulatory turning point. Parliament is advancing a package of foreign-buyer restrictions at the exact moment external demand is still setting the pace in key districts. When policy tightening collides with late-cycle momentum, markets rarely move in a straight line: volumes can surge before implementation, then fragment by product type, buyer nationality, and location risk.

What the 2026 Restriction Package Actually Changes

According to linked parliamentary coverage in this Theme and its source news records, the proposed framework combines several drafts into one enforceable regime. The practical core is clear: tighter limits on what non-EU buyers can acquire, where they can acquire it, and how long they must hold it. The package includes restrictions near military and strategic zones, explicit constraints on agricultural and forest-linked assets, a 200 square meter cap for specific residential acquisition pathways, and retention logic around a five-year horizon. In market terms, that is not a marginal tax tweak; it is an inventory-access rule change.

The timing matters more than the wording. The legislative sequence has been transparent enough to trigger a pre-implementation behavior shift: foreign buyers and intermediaries accelerate decision cycles before hard constraints become binding. This is consistent with prior policy windows in Mediterranean markets, where announcement effects often arrive earlier than enforcement effects. For brokers and developers, the real issue is not whether demand disappears; it is whether demand migrates into fewer, policy-compatible asset classes.

Demand Pressure Is Real: Shares and Volumes Confirm It

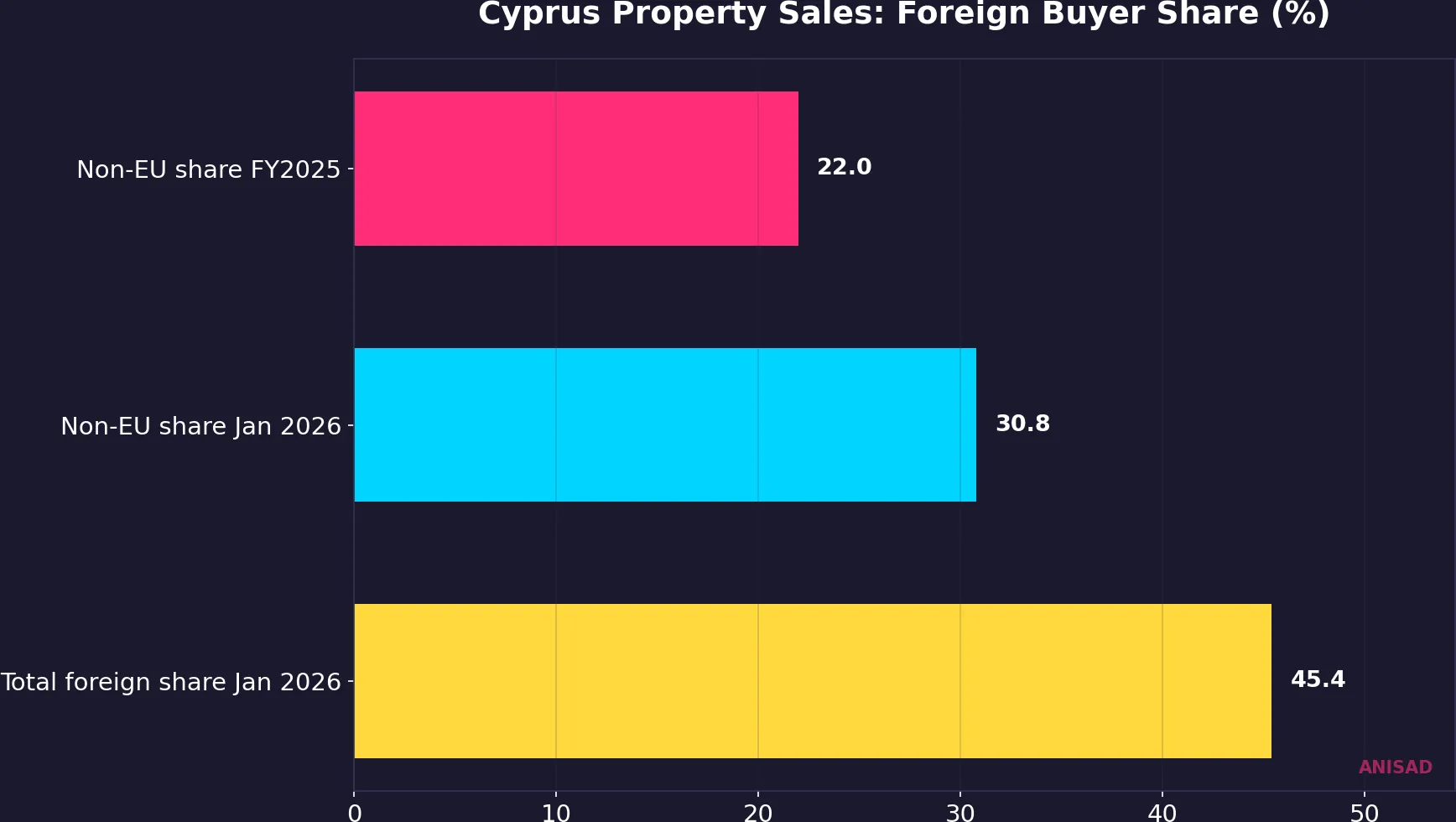

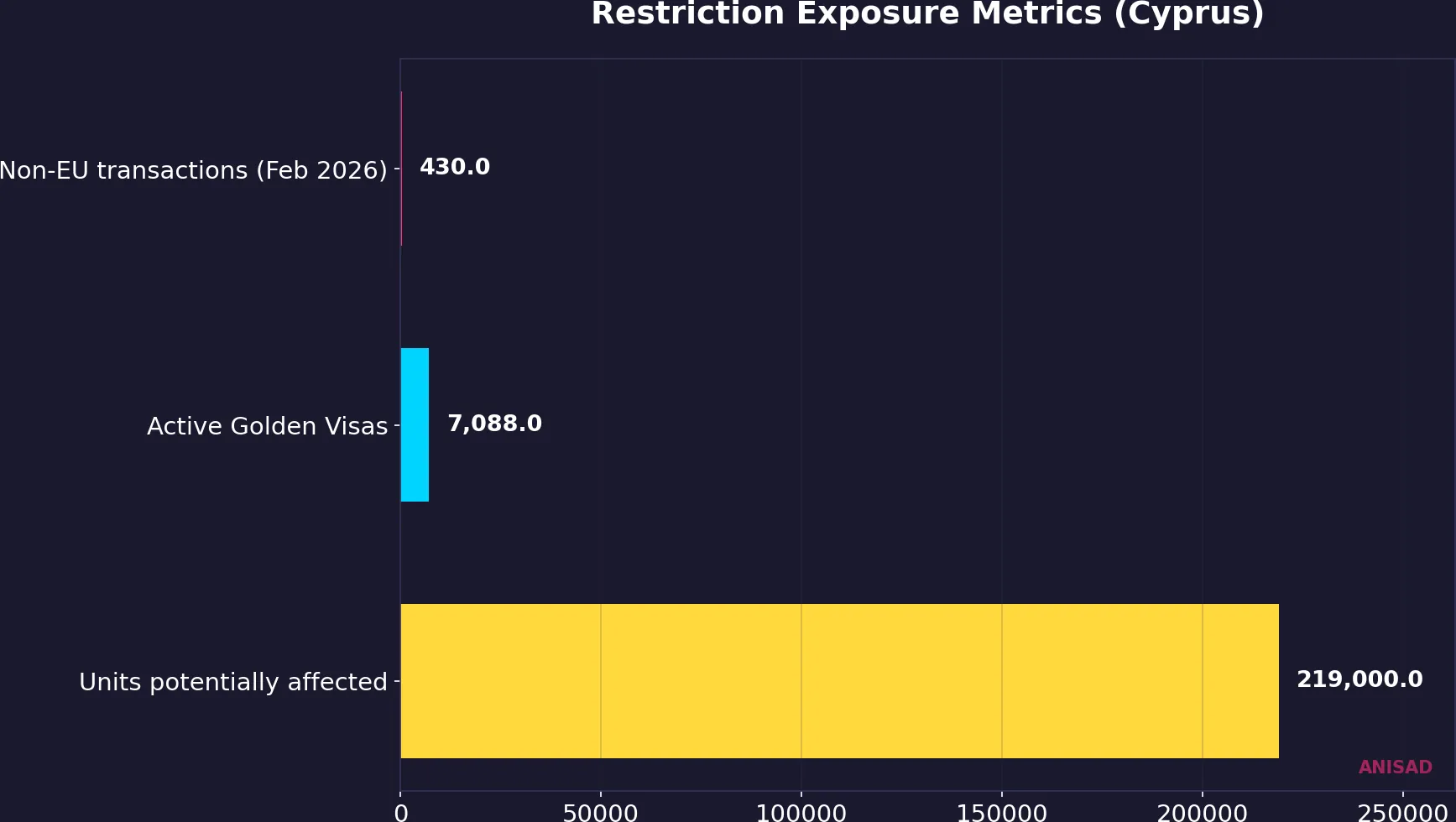

The linked Market Signals for this theme show why lawmakers moved now. Non-EU buyer participation rose from 22.0% in FY2025 to 30.8% in January 2026, while total foreign-buyer share reached 45.4% in the same month. That is not a niche flow anymore; it is market-shaping scale. Additional records in the same theme show foreign buyer dominance around 50% in high-interest land and coastal hotspots, plus 430 monthly non-EU transactions in February 2026. Even without aggressive assumptions, this is sufficient to alter local affordability narratives and political tolerance for open-ended access.

Importantly, these percentages must be interpreted as transaction-share signals, not direct proof of identical price growth across all submarkets. But the policy implication remains: once foreign share approaches half the market in headline periods, regulators can justify intervention under both affordability and national-security arguments. In Cyprus, the security dimension adds legal urgency that pure price concerns alone often lack.

Second-Order Effects: Product Rotation, Not Simple Demand Collapse

The highest-probability scenario is rotation, not evaporation. Buyers facing restricted land pathways typically move toward already-permitted apartment inventory, mixed-use structures with clearer ownership transparency, and developer-backed products with lower legal friction. That supports near-term resilience in specific urban segments even if total cross-border appetite cools. At the same time, assets exposed to boundary restrictions or ambiguous zoning can reprice sharply due to uncertainty premiums.

Signals linked to this theme also indicate 219,000 housing units potentially within the broader policy impact envelope, alongside 7,088 active Golden Visa permits and a EUR 300,000 minimum investment benchmark. These figures are different in nature (stock, flow, and threshold), but together they show the size of the policy interface between migration capital and domestic supply.

Who Benefits, Who Is Exposed

- Potential beneficiaries: local first-time buyers in segments where speculative foreign bids previously dominated.

- Potential beneficiaries: developers with compliant urban apartment pipelines and transparent ownership structures.

- Potential beneficiaries: legal and advisory firms specializing in structuring, disclosure, and cross-border compliance.

- Potentially exposed: land-focused strategies dependent on non-EU discretionary buyers near restricted zones.

- Potentially exposed: brokers concentrated in products likely to face screening or holding-period frictions.

- Potentially exposed: investors relying on rapid resale dynamics that conflict with retention requirements.

6-24 Month Outlook: Three Signals to Track

- Pre-implementation spike versus post-implementation normalization: if monthly non-EU transactions overshoot before enforcement, expect a visible payback period afterward.

- District-level dispersion: monitor whether demand re-concentrates in policy-compatible urban stock rather than exiting Cyprus entirely.

- Execution quality: the operational burden of beneficial ownership checks and permit pathways will determine whether the law becomes a precise filter or a broad brake.

The strategic mistake would be to read this as a binary story of open versus closed market. The evidence points to a segmented repricing cycle: higher compliance premium, wider spread between clean and constrained inventory, and faster capital rotation by informed buyers. If implementation is strict but predictable, institutional investors may adapt quickly. If implementation is inconsistent, liquidity could thin in exactly the segments the state wants to stabilize.

Bottom Line

Cyprus is no longer discussing whether to intervene in foreign-buyer access; it is defining the operating manual. For 2026, the trade is not simply “foreign demand up or down.” The trade is legal certainty versus legal friction, and which assets remain inside the compliant channel. In that environment, due diligence speed, structure quality, and district-level policy mapping become more important than headline market optimism.

Data sources: Cyprus Parliament and committee coverage via Cyprus Mail linked records (Mar-Apr 2026), Department of Lands and Surveys transaction-share signals linked to Theme Cyprus Foreign Buyer Restrictions 2026, Migration Department / Golden Visa signal records linked to the same Theme, FDI screening notices from Cyprus Ministry of Finance linked records