Europe's rental markets are undergoing a regulatory transformation unseen since the post-war era. From Spain's punitive tax measures against landlords to the EU's pan-European short-term rental registration mandate, governments across the continent are systematically dismantling the investor-friendly frameworks that fueled a decade of rental yields. For property investors in Cyprus and the wider Mediterranean, this wave carries both a warning and an opportunity.

The Regulatory Trigger: Why Now?

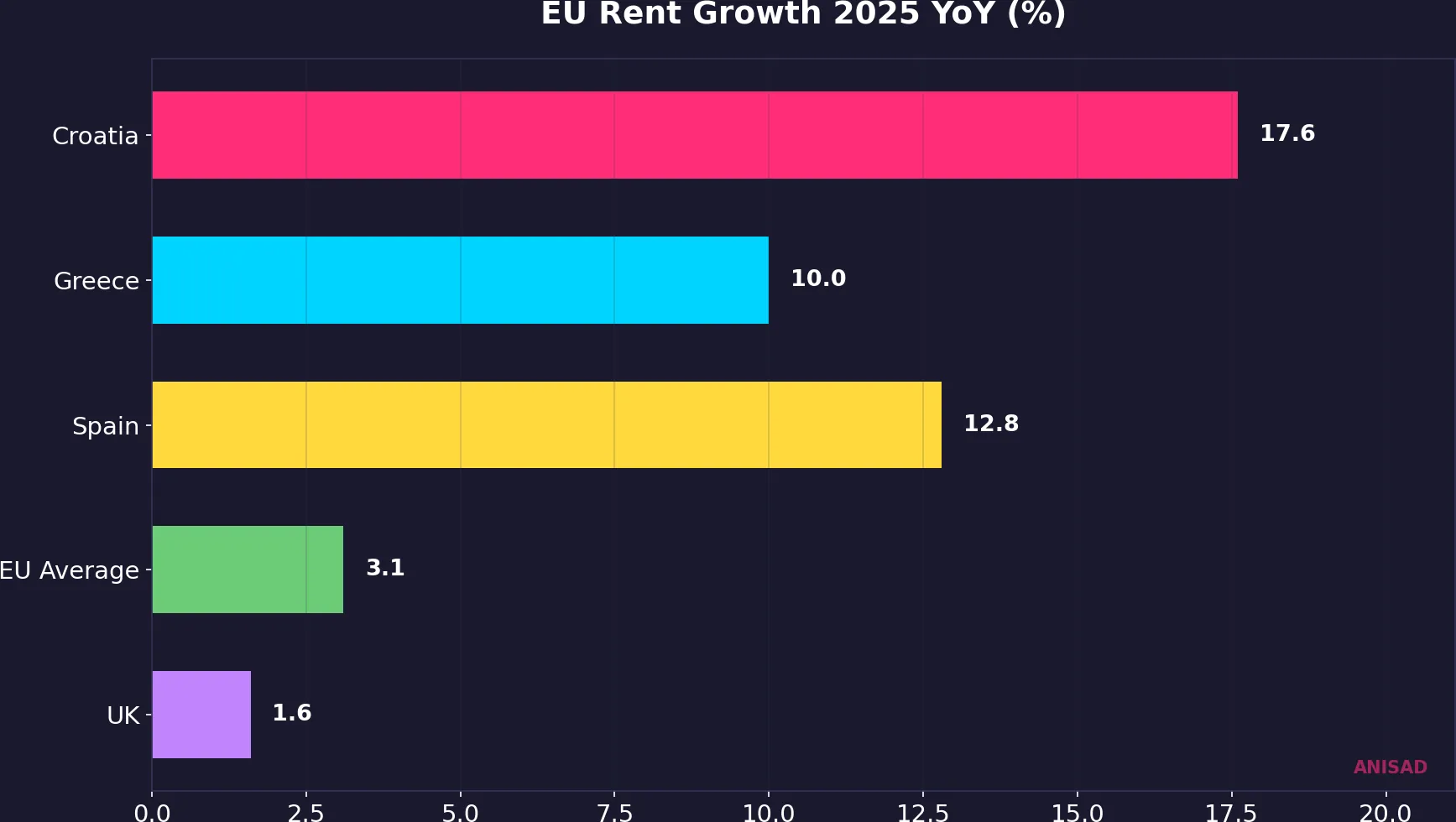

The answer is straightforward: rents became politically unsustainable. EU average rents rose 3.1% in 2025, but this headline figure masks extreme national divergences. Croatia's rents surged 17.6%, Greece posted 10% growth, and Spain's housing costs jumped 12.8% year-over-year by end-2025 (Eurostat, Euronews 2025 analysis). The UK — long a bellwether for English-speaking rental markets — finally hit its affordability ceiling in Q1 2026, with rents flatting at £1,370/month outside London for the first time since 2017 (Rightmove data). A record 26% of UK listings now show price cuts.

When rents consume 40-60% of median household income across major European cities, regulatory intervention becomes politically inevitable. The question is no longer whether governments will act, but how aggressively — and Spain is providing the template.

Spain: Europe's Regulatory Laboratory

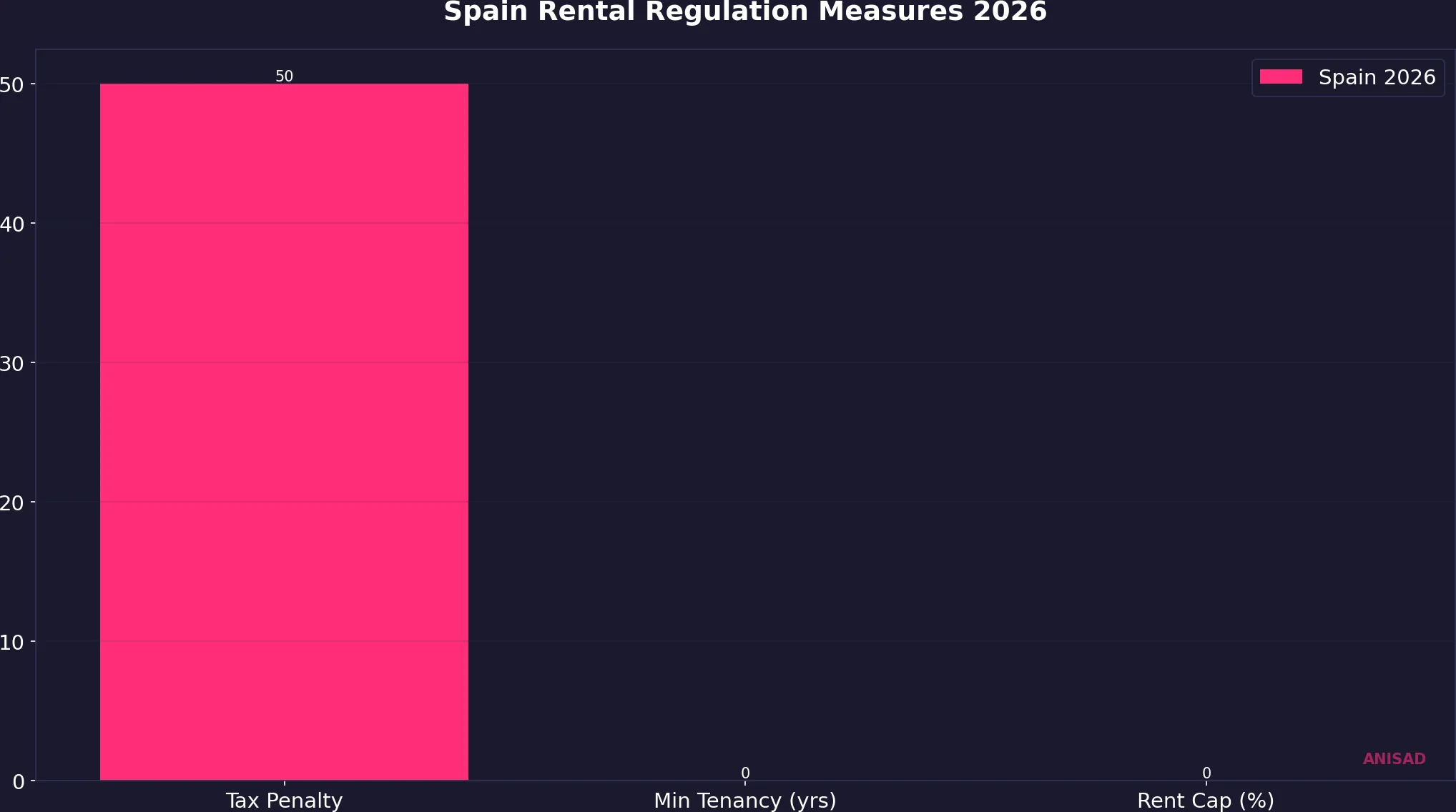

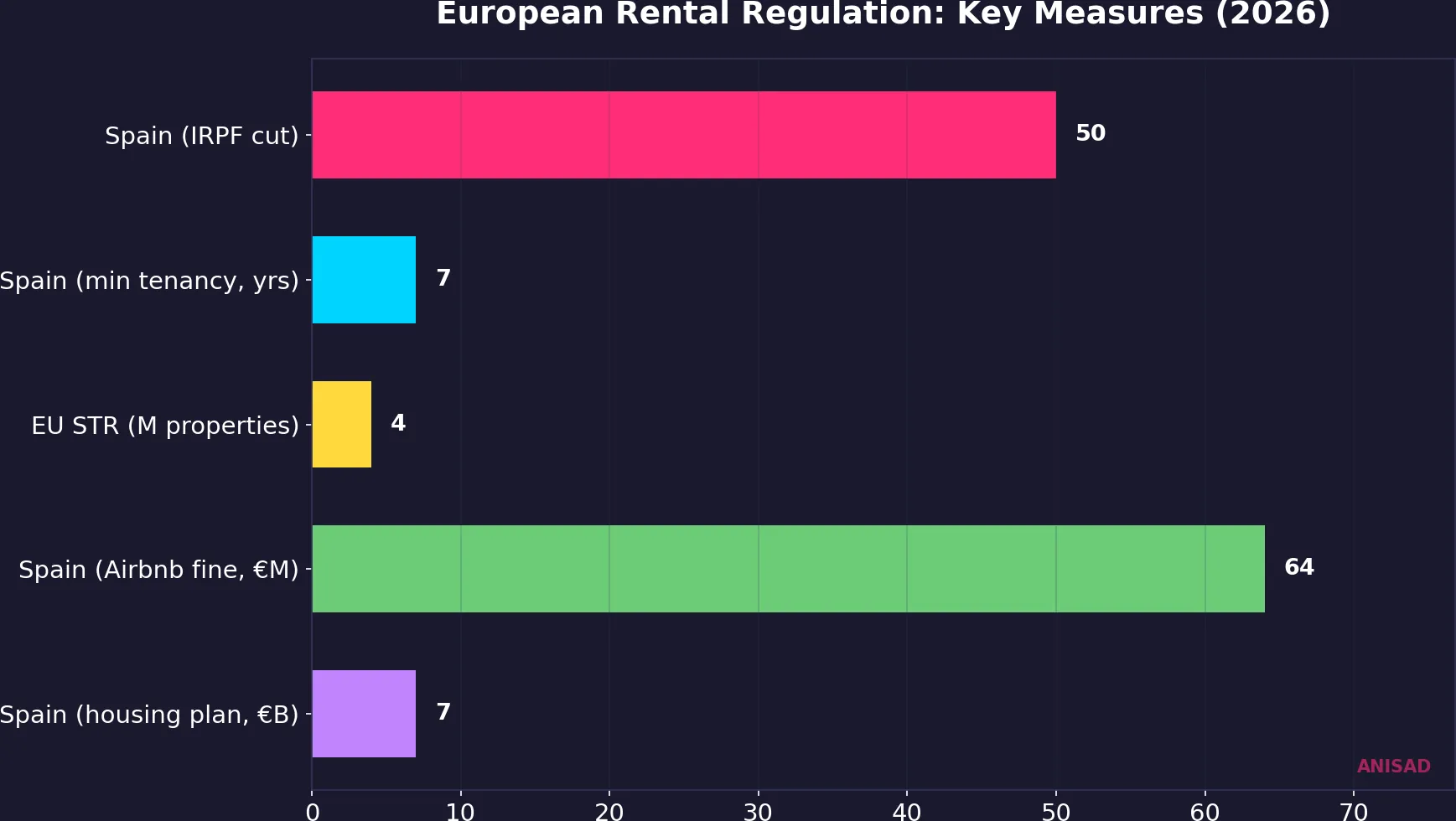

Spain has enacted the most comprehensive tenant protection package in the EU, deploying fiscal punishment, mandatory tenancy extensions, and emergency decree powers in rapid succession. The 2026 fiscal reform reduces the standard 50% IRPF tax deduction on rental income for any landlord who raises rent at contract renewal. This mechanism converts rent increases into an automatic tax penalty — a first in European housing policy.

The Ley de Arrendamientos Urbanos (LAU) now mandates 5-year minimum tenancies for private landlords and 7-year minimum tenancies for corporate landlords. Combined with Catalonia's deployment of 56 SPER anti-eviction professionals across 5 zones, Spain has constructed an institutional apparatus that makes tenant displacement structurally difficult.

Most significantly, Real Decreto-ley 8/2026, enacted in April 2026, forces 2-year lease extensions and imposes a 2% rent cap effective through December 2027 — justified by the Iran-Gulf conflict. This is Spain's third crisis-triggered rental intervention since COVID-19, establishing a pattern where each geopolitical shock ratchets tenant protections higher without sunset mechanisms that actually restore landlord flexibility.

EU-Wide Intervention: From National Policies to Supranational Mandates

The European Parliament's March 2026 resolution — adopted 367-166 with 84 abstentions — demands 10 million new homes across the EU, a 60-day construction permit cap, and state aid relaxation for social housing. While non-binding, this resolution signals Brussels' willingness to set housing benchmarks that individual member states will face political pressure to meet.

The EU's Short-Term Rental Regulation (EU 2024/1028), effective May 20, 2026, mandates all 27 member states to establish Single Digital Entry Points for STR registration. An estimated 4 million properties will require mandatory registration across the EU — creating unprecedented transparency into a sector that previously operated in regulatory shadows. For the first time, governments will possess the data to enforce STR restrictions systematically rather than selectively.

Greece has already acted aggressively: effective January 2026, all rent payments must go through bank transfers, eliminating the estimated 30-40% of transactions that historically evaded taxation. Athens also introduced 3-year tax holidays for landlords who convert short-term rental properties to long-term leases (Codes 64-67) — a fiscal carrot paired with a compliance stick.

The Enforcement Escalation: Airbnb's €64M Fine

A Spanish court ordering Airbnb to pay a €64 million fine — and refusing to suspend the sanction — marks a regulatory inflection point. This is among the largest penalties against a short-term rental platform in European history. The enforcement precedent is clear: EU regulators are moving from rule-setting to active punishment of non-compliance. Other Mediterranean markets, including Cyprus, face pressure to demonstrate equivalent enforcement capacity or risk being characterized as regulatory havens.

Spain's €7 billion public housing plan, approved in April 2026, triples housing investment over 4 years. Forty percent targets new public stock construction, 30% goes to renovation, and the plan prevents privatization of subsidized housing. The scale of fiscal commitment signals that the regulatory intervention is not temporary — it represents a structural rebalancing of the landlord-tenant relationship.

Implications for Cyprus and Mediterranean Investors

Cyprus stands as the last major Mediterranean market without comprehensive rental or STR regulation. While Spain punishes rent increases and Greece mandates bank-only payments, Cyprus's STR market processed 3.1 million guest nights in peak summer 2025 without equivalent oversight. This regulatory arbitrage window is narrowing rapidly as the EU STR mandate takes effect.

The investment calculus is shifting. Markets with aggressive tenant protections — Spain, Portugal, increasingly Greece — are seeing capital redirect toward jurisdictions with more predictable regulatory environments. For Cyprus, this creates a dual dynamic: short-term capital inflows from investors fleeing regulated markets, combined with long-term regulatory convergence pressure from Brussels that will eventually constrain the same freedoms attracting that capital.

The UK Precedent: What Happens at the Affordability Ceiling

The UK market provides a preview of what awaits Mediterranean markets that resist regulation. After rents rose more than 30% since 2020, the market self-corrected in Q1 2026: year-on-year growth dropped to 1.6% (the lowest since 2018), 26% of listings show price cuts, and enquiries per property fell from 11 to 8. Supply increased 3% year-over-year to the highest level since 2021. Even without Spain-style government intervention, market forces eventually impose their own discipline. The question for investors is whether government action arrives first — compressing yields suddenly — or market correction arrives gradually.

What to Watch: 6-24 Month Outlook

The EU STR registration deadline of May 20, 2026 is the immediate catalyst. Once 4 million properties enter a transparent registry, enforcement actions will accelerate across all member states. Cyprus must implement its Single Digital Entry Point or face infringement proceedings — and implementation will expose the full scale of its unregulated STR sector.

Spain's 2% rent cap runs through December 2027, with no political appetite for reversal given the ongoing Iran conflict justification. Any new geopolitical disruption provides the template for further emergency measures. Greece's bank-only payment mandate will generate tax revenue data by Q3 2026 that other countries will study as a compliance model.

For property investors, the strategic imperative is clear: price regulatory risk into Mediterranean acquisition decisions today. Markets offering high yields without tenant protections are not under-regulated paradises — they are pre-regulated markets where the intervention timeline is measured in quarters, not decades.

Data sources: Eurostat — House Price Index and Rental Data (prc_hpi_q), Q4 2025, Euronews — European Rent Surge Analysis 2025, Spanish Government — Real Decreto-ley 8/2026 (BOE), Ley de Arrendamientos Urbanos (LAU) — tenancy duration reform, EU Regulation 2024/1028 — Short-Term Rental Data Collection, European Parliament — Housing Crisis Special Committee Resolution, March 2026, Rightmove / The Guardian — UK Rental Market Data Q1 2026, Greek Government — Rental Payment Bank Transfer Mandate (Codes 64-67), Spanish Court — Airbnb €64M Penalty Ruling, Knight Frank — European Rental Market Report 2025