A fatal building collapse in Germasogeia has moved construction safety from a specialist engineering topic into the center of Cyprus real-estate strategy. For years, the dominant narrative was expansion: permits up, units up, and external capital still interested in Cyprus as a Mediterranean allocation. The collapse changed the frame. Investors, lenders, and buyers are now asking a different question: can supervisory capacity scale as quickly as development volume?

That question matters because market confidence is not built only on demand metrics. It is built on the credibility of the entire delivery chain: design review, site supervision, materials quality, contractor governance, inspection cadence, and legal accountability after incidents. When one part of that chain fails visibly, all adjacent components are repriced in participants' risk models.

Why this incident is structurally different

Cyprus has seen building-quality disputes before, but this case landed in a period of active construction acceleration and international buyer sensitivity. That combination gives the event structural significance. It is no longer a local legal story; it is a market-quality story with implications for underwriting, insurance, and project-level liquidity.

In a slower market, isolated incidents can remain isolated. In a fast-growth market, incidents can become proxies for wider governance concerns. This is why the next 6-12 months are critical: either Cyprus demonstrates credible enforcement and quality controls, or the market absorbs a persistent risk premium that raises the cost of capital across the board.

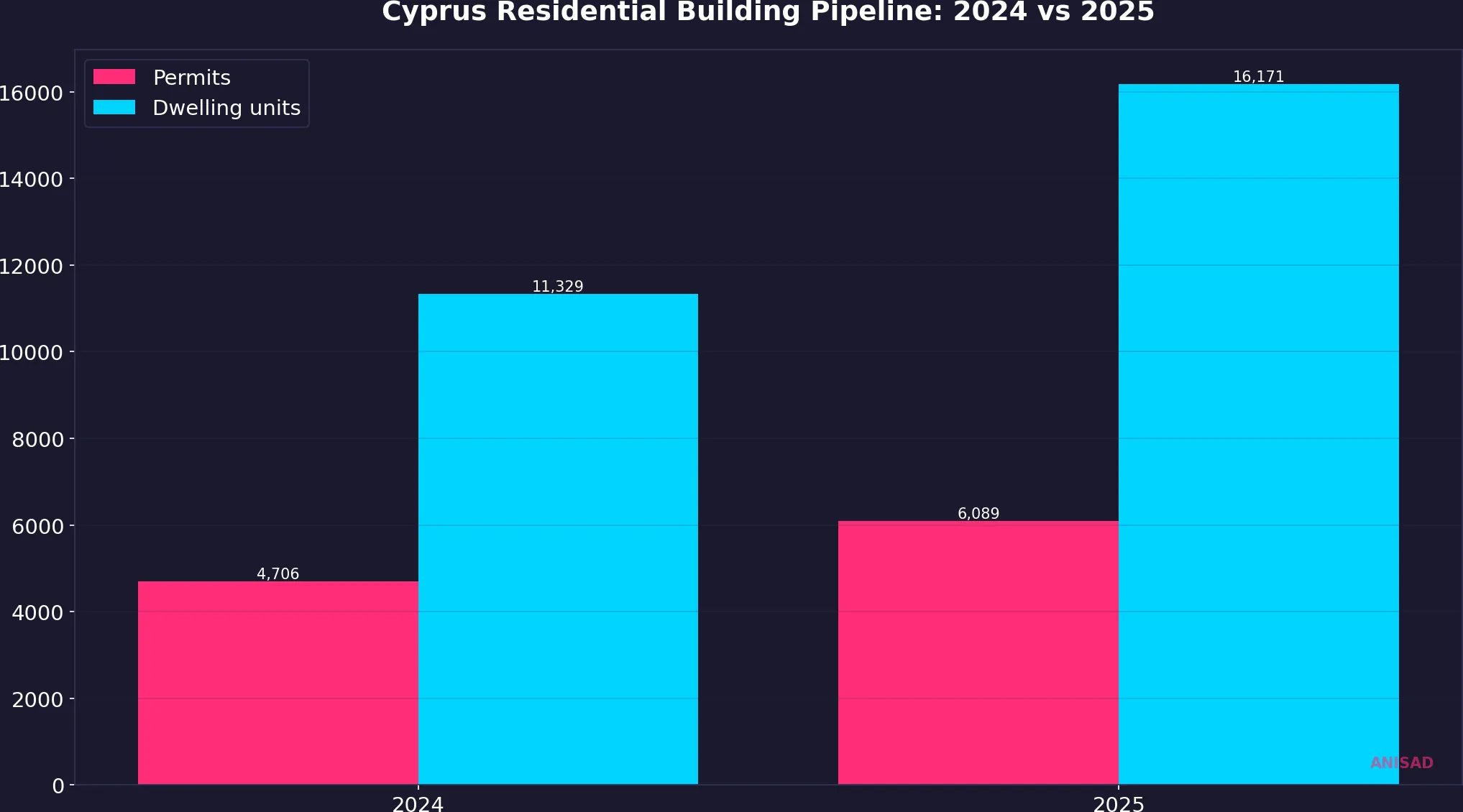

The volume context: official data confirms expansion

Official CYSTAT building-permit data confirms that this safety debate is happening during a strong expansion phase, not a contraction. Residential building permits increased from 4,706 in 2024 to 6,089 in 2025, while permitted dwelling units increased from 11,329 to 16,171. That scale change is substantial: it implies more active sites, more subcontracting layers, and more pressure on technical supervision systems.

- CYSTAT: Residential building permits rose from 4,706 (2024) to 6,089 (2025), a 29% year-over-year increase.

- CYSTAT: Residential dwelling units in permits increased from 11,329 to 16,171, a 43% year-over-year increase.

- Theme-linked incident records report up to 2 confirmed fatalities in the Germasogeia collapse event set.

Permit growth itself is not a problem; in fact, it reflects supply response and investment activity. The risk emerges when approval and delivery speed outpace monitoring and enforcement resources. In that environment, a single failure can trigger broad re-evaluation of project quality, especially in markets where off-plan sales and international buyer confidence are important.

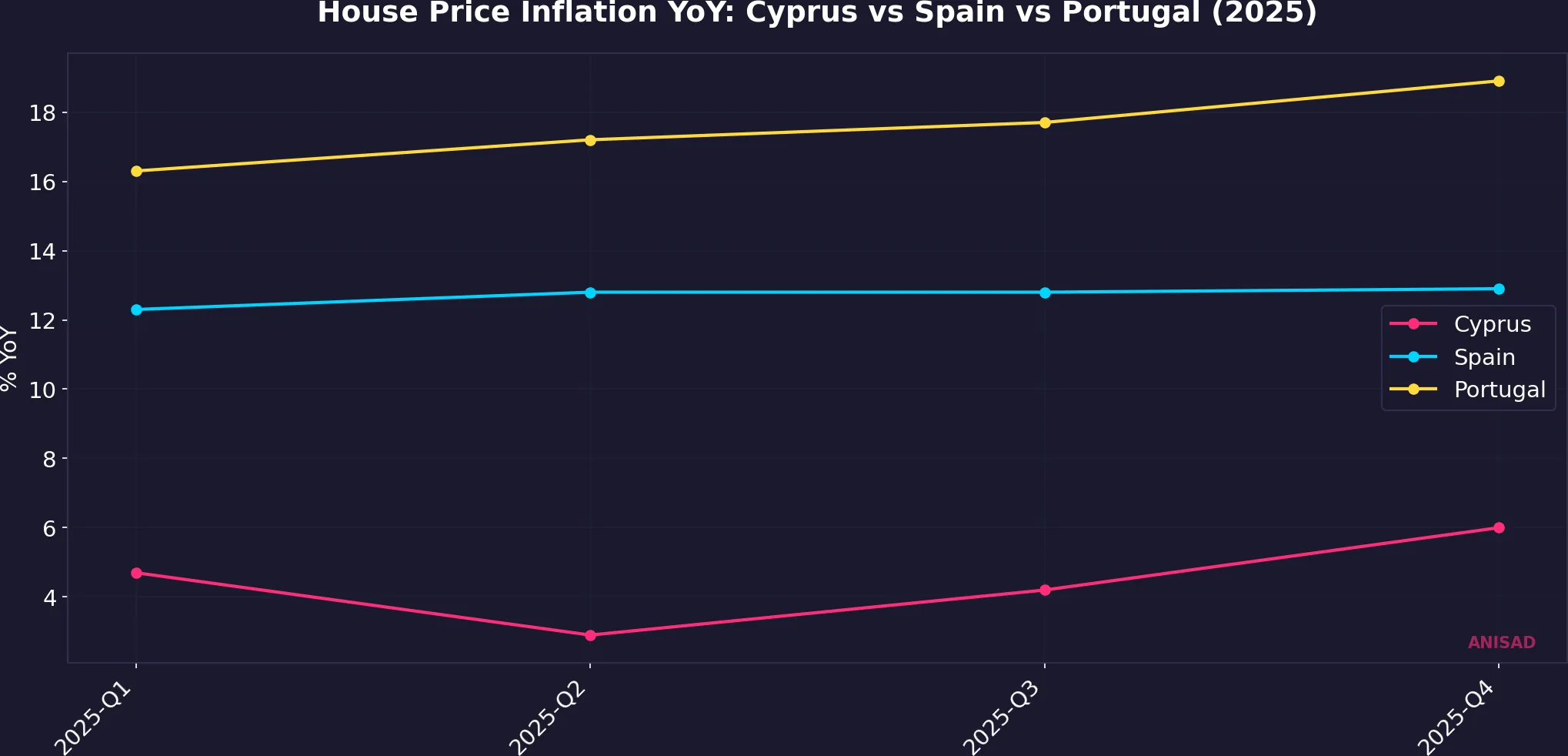

Price momentum remains positive, but risk is becoming selective

Eurostat house-price data shows Cyprus still in positive annual growth through 2025, with quarterly year-on-year readings of 4.7%, 2.9%, 4.2%, and 6.0%. At the same time, Spain and Portugal posted materially higher annual rates in the same period. This means Cyprus is no longer competing only on momentum; it is increasingly competing on execution quality and perceived governance reliability.

For capital allocators, this creates a practical filter. Projects in jurisdictions with cleaner quality controls and clearer accountability frameworks can attract funding even when headline growth rates are lower. Projects in ambiguous governance environments may still close, but with tighter covenants, stricter drawdown conditions, and higher pricing for construction and completion risk.

How financing and insurance behavior may change

Banks and private lenders are likely to respond first through process, not public statements. Expect deeper technical due diligence, stronger requirements for independent engineering certifications, and closer milestone verification before tranche releases. For leveraged developers, this translates into slower cash conversion cycles and potentially higher carrying costs if documentation pipelines are weak.

Insurers face a similar adjustment. A visible structural incident in an expansion zone can shift actuarial assumptions, especially if legal outcomes imply shared liability or weak preventive controls. If premiums increase on large or complex projects, the impact flows directly into end-pricing and margin pressure, reinforcing the advantage of operators with better safety governance.

Stakeholder map: winners, losers, and neutral actors

Potential winners include developers with robust compliance systems, engineering consultancies offering third-party verification, and institutional buyers willing to pay for transparency. Potential losers include speed-first projects with thin QA processes, contractors with weak documentation culture, and speculators relying on compressed completion timelines.

Homebuyers and long-term residents can benefit if the policy response is substantive rather than symbolic. Better quality control reduces tail-risk events and improves trust in new-build stock. However, if tighter oversight arrives without process modernization, delivery bottlenecks can increase affordability pressure through delayed completions.

Policy execution risk: announcement versus implementation

The market should distinguish between regulatory announcements and operational implementation. Announcing tougher rules can calm headlines, but only sustained enforcement changes risk pricing. Key indicators to monitor include inspection staffing levels, inspection frequency per project phase, publication of enforcement outcomes, and time-to-resolution for serious violations.

If Cyprus demonstrates measurable improvements on those indicators, the collapse can become a policy inflection point that strengthens long-term market credibility. If implementation remains uneven, confidence recovery may be shallow and concentrated in only the most established developers and submarkets.

Forward scenarios for the next 6-24 months

Base case: targeted tightening with better execution. In this path, permit activity continues but project governance quality becomes a larger determinant of financing access and absorption speed. Market activity remains positive, but valuation dispersion widens between high-trust and low-trust projects.

Downside case: reactive regulation with weak operational follow-through. Here, the market absorbs uncertainty without gaining safety certainty, increasing legal friction, financing cost, and buyer hesitation in selected locations. Volume does not necessarily collapse, but time-to-close and project risk premia increase.

Upside case: rapid institutional learning. Regulators, municipalities, lenders, and developers align around verifiable safety standards and transparent reporting. Cyprus then reframes the incident from a reputational shock to a proof point of governance maturity, which can support medium-term competitiveness in Mediterranean capital allocation.

In the next cycle, the market may reward documented quality assurance more than pure construction speed.

Data sources: CYSTAT-DB: Building Permits annual table (residential buildings, 2024-2025), CYSTAT-DB: House Price Index quarterly table (base 2015=100), Eurostat prc_hpi_q: annual house-price change (Cyprus, Spain, Portugal), Linked Real Estate News records covering the Germasogeia collapse and subsequent policy debate