Spain proved in 2025 that you do not need to ban foreign property buyers to drive them away — you just need to threaten convincingly enough. Prime Minister Pedro Sánchez's campaign against non-EU buyers, complete with a floated 100% purchase tax and outright ban proposals, triggered a 17% year-on-year drop in non-EU, non-resident purchases despite zero legislation being enacted. The episode is now the Mediterranean's most vivid case study in how political rhetoric alone functions as de facto capital control — and it carries direct lessons for every competing destination, Cyprus included.

The Sánchez Playbook: Rhetoric as Policy

In January 2025, Sánchez announced a package of housing affordability measures that targeted foreign buyers as a symbolic villain. The proposals included a 100% tax on property purchases by non-EU, non-resident buyers and a potential outright ban. Neither measure became law. Spain's fragmented parliament, where Sánchez leads a minority government, could not produce the legislative majorities needed. The Golden Visa program, which granted residency to property investors spending above €500,000, was officially terminated in April 2025 — but this had been telegraphed since mid-2023 and was already priced in by the market.

What made the Spanish situation unusual was the scale of the gap between signaling and action. The government repeatedly raised the prospect of severe restrictions, generated international media coverage, and created genuine uncertainty among foreign buyers — all without passing a single restrictive law. The Catalan regional government added its own pressure through Law 11/2025, which expanded public intervention mechanisms in high-demand housing areas, though it stopped short of direct foreign buyer restrictions. Barcelona's city council discussed separate proposals to limit non-resident purchases. The cumulative effect was a layered political message: foreign capital is unwelcome.

Measuring the Damage: The Numbers Behind the Exodus

The market response was immediate and measurable. Total non-resident foreign property purchases in Spain fell 9.4% year-on-year in 2025, dropping from 58,247 homes to 52,781. Within that decline, the non-EU, non-resident segment — the specific target of Sánchez's rhetoric — suffered a steeper 17% decline. The geographic distribution of the damage concentrated in Spain's traditional foreign buyer hotspots: the Balearic Islands recorded an 8.3% drop, the Canary Islands fell 9%, and Valencia declined 5.2%.

The irony embedded in these numbers is the scale mismatch between the political narrative and the actual market footprint. Non-EU, non-resident buyers represent approximately 2% of Spain's total housing market and about 11% of the foreign buyer segment. The housing affordability crisis that Sánchez invoked to justify the campaign is driven overwhelmingly by domestic demand, limited supply, and financialization — not by a sliver of non-EU purchases. Yet that 2% share generated enough political currency to sustain months of international headlines and create a measurable capital flight.

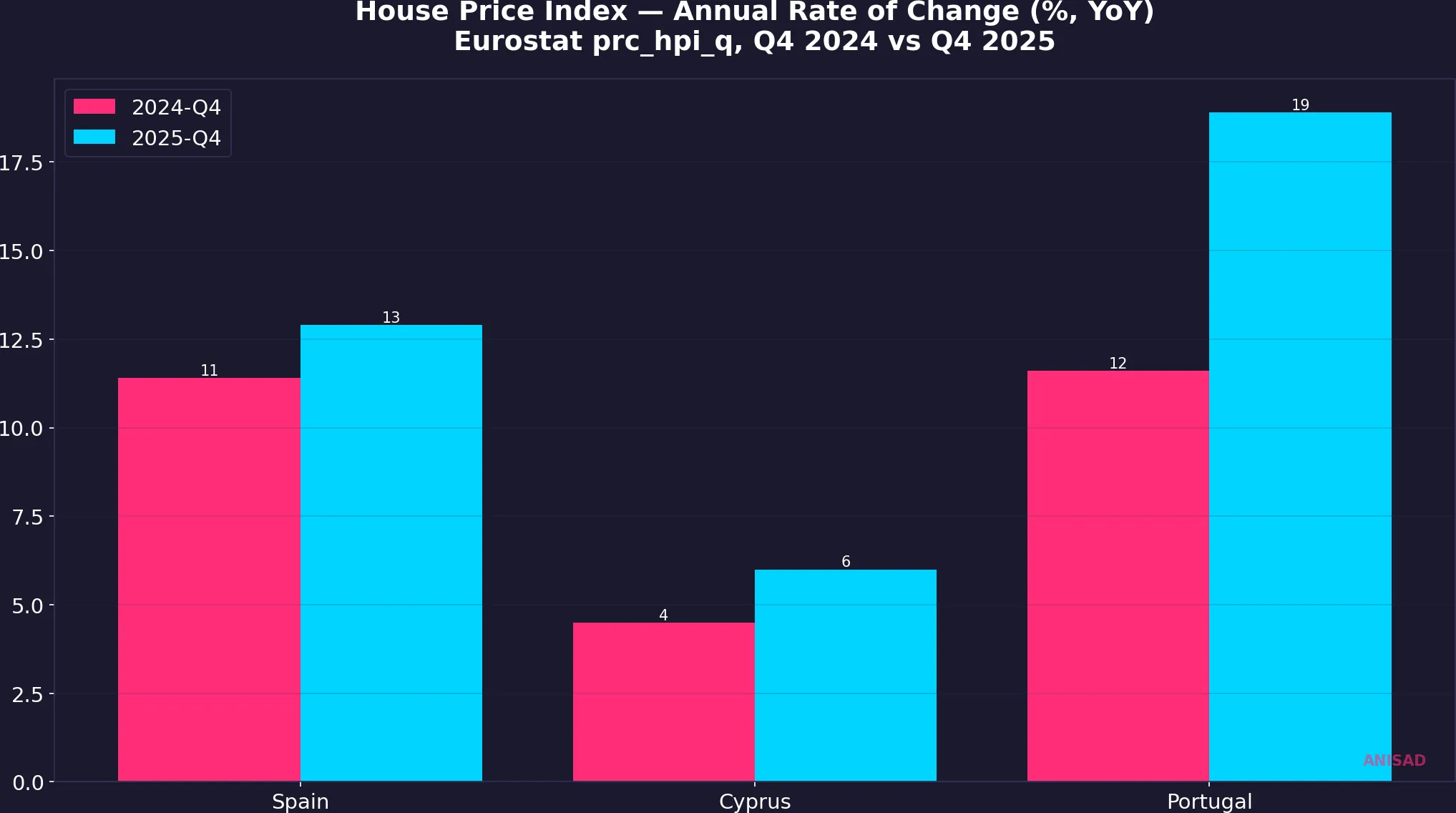

Where the Capital Goes: Mediterranean Musical Chairs

Investment capital displaced from Spain does not evaporate — it redirects. The primary beneficiaries are Mediterranean markets that maintain stable, investor-friendly regulatory environments. Portugal, despite having its own Golden Visa restrictions since October 2023, continues to attract capital through its Non-Habitual Resident (NHR) successor scheme and recorded house price growth of 18.9% year-on-year in Q4 2025, the highest in the EU according to Eurostat. Greece has actively positioned itself as an alternative, raising its Golden Visa threshold to €800,000 in Athens and Thessaloniki while keeping lower thresholds in secondary markets. Cyprus, with its permanent residency pathway via property investment (minimum €300,000), stands to capture a share of the redirected flows.

The Eurostat House Price Index reveals diverging trajectories across Mediterranean peers. Spain's HPI grew 12.9% year-on-year in Q4 2025 — strong domestic demand counterbalancing the foreign buyer retreat. Cyprus posted a more moderate 6.0% annual increase, while Portugal surged to 18.9%. These figures suggest that Spain's anti-foreign-buyer stance has not dented its domestic price growth but has created opportunity windows for competing destinations to absorb displaced international demand.

The Cyprus Parallel: Risk and Opportunity

For Cyprus, Spain's experience is simultaneously a warning and an invitation. The warning: similar populist rhetoric around foreign buyers has surfaced in Cypriot political discourse, driven by genuine affordability concerns. If a Cypriot government were to adopt Sánchez-style signaling — floating restrictions without legislating them — the precedent suggests a meaningful capital retreat would follow, despite Cyprus's small-scale market being even more vulnerable to sentiment shifts than Spain's.

The invitation: Cyprus currently benefits from the perception of regulatory stability relative to Spain. The permanent residency program remains operational, property ownership rights for non-EU nationals are legally protected, and the government has shown no appetite for punitive taxation of foreign buyers. Every month that Spain's political uncertainty persists reinforces Cyprus's competitive position as a safe Mediterranean harbor for international property capital. The CYSTAT House Price Index, which reached 152.93 (base 2015=100) in Q2 2025 with a 4.2% year-on-year increase, reflects steady rather than explosive growth — a profile that appeals to long-term investors wary of Spanish-style political volatility.

The Phenomenon: Rhetoric as De Facto Capital Control

Spain's 2025 episode names a new phenomenon in European housing markets: political signaling as de facto capital control. In traditional economic frameworks, capital controls are formal policy instruments — taxes, quotas, licensing requirements. Spain demonstrated that informal tools — public statements, leaked policy proposals, sustained media campaigns — can achieve comparable results without any legislative cost. The 17% decline in non-EU purchases was not caused by regulation; it was caused by uncertainty about regulation that never materialized.

This pattern is likely to replicate. Housing affordability is a top-tier political issue across the EU. Targeting foreign buyers offers governments a visible scapegoat that deflects from structural supply failures, restrictive zoning, and domestic speculation — none of which are electorally easy to address. The Spanish model shows that rhetorical intervention alone can produce measurable market shifts, making it an attractive template for populist housing platforms across the continent.

What to Watch: Leading Indicators for Capital Redirection

Investors monitoring Mediterranean capital flows should track several signals. First, watch Spanish parliamentary activity: any revival of the 100% tax proposal or formal legislative drafting would escalate from rhetoric to genuine risk, potentially accelerating capital outflows beyond the current trajectory. Second, track Canary Islands EU authorization requests to limit non-primary-residence purchases — if Brussels grants this precedent, other Spanish regions and potentially other EU member states will follow. Third, monitor Cyprus's own political discourse around foreign buyers: the moment affordability rhetoric shifts from general concern to targeted policy proposals, the Sánchez Effect applies in reverse.

On the opportunity side, non-EU buyer transaction volumes in Cyprus, Greece, and Croatia serve as the direct measure of capital redirection. If Spain's political posture persists through 2026, the capital displacement should become structural — buyers who explored alternatives during the uncertainty period are unlikely to return even if Spain eventually moderates its rhetoric.

Conclusion

Spain's anti-foreign-buyer campaign is the Mediterranean's most consequential housing policy experiment of 2025 — and no policy was actually enacted. The 17% decline in non-EU purchases, driven entirely by political signaling, establishes a new playbook for governments seeking to demonstrate housing market intervention without legislative risk. For Cyprus, the lesson is binary: maintain regulatory stability and absorb the redirected capital, or follow Spain's rhetorical path and watch the same capital flee. The Mediterranean property market has entered a competitive era where investor confidence is the primary differentiator — and Spain just demonstrated how quickly that confidence can be destroyed.

Data sources: Spanish Property Insight — "Non-EU foreign buyers take a hit in 2025 after political backlash" (April 2026), Spanish Property Insight — "Has foreign demand for Spanish property peaked?" (May 2026), Reuters — "Spain's PM Sánchez floats ban on non-EU citizens buying properties" (January 2025), Eurostat prc_hpi_q — House Price Index, annual rate of change, Q4 2024 and Q4 2025, CYSTAT — House Price Index (Base Year 2015=100), Quarterly, Q2 2025, Spanish Notaries — Non-resident foreign purchase transaction data, 2024–2025