After twenty years and three terminated contracts, the Larnaca port and marina project is edging closer to a real breakthrough. The Cyprus government has adopted a new Growthfund-backed strategy that splits the port and marina into financially independent developments — sidelining a EUR 1.2 billion joint bid and signalling a pragmatic pivot away from the mega-deal model that failed three times. For property investors, the timing matters: Larnaca remains the cheapest coastal district in Cyprus, and the window to buy ahead of confirmed infrastructure may be narrowing.

The Twenty-Year Saga: Why Larnaca Is Still Waiting

The Larnaca port and marina redevelopment is the most prominent stalled infrastructure project on the island. Since the early 2000s, three concessions have been awarded and subsequently terminated, the most recent being Kition Ocean Holdings. Each failure eroded investor confidence and delayed the district's transformation into a premium waterfront destination. The pattern was always the same: an ambitious single-entity concession, overpromising on scope, underdelivering on financing.

In February 2026, Transport Minister Alexis Vafeades presented a Growthfund study to the Larnaca Development Committee that proposed a fundamentally different approach. Rather than a single anchor investor bearing the full financial and operational weight, the recommendation is to develop the port and marina as separate, self-sustaining projects. This is not a cosmetic restructuring — it redefines the risk-sharing model and opens the door to phased, modular development rather than an all-or-nothing gamble.

What the New Strategy Looks Like

The separated development model envisions a minimum of 600 yacht berths accommodating vessels up to 115 metres, a beach hotel, a yacht club, a cruise terminal, and supporting tourism infrastructure deployed across four phases. The financial component of the Growthfund study was due in mid-April 2026, representing the most concrete decision point in the project's history. In May 2026, the government escalated further: the Deputy Ministry of Tourism announced a national 2035 strategy to position Cyprus as a luxury yachting hub, broadening the infrastructure thesis from a Larnaca-specific initiative to an island-wide maritime tourism pivot.

This government-level commitment provides a policy backstop that previous concession holders lacked. Developers can now cite an official 2035 strategy in investor presentations, de-risking premium waterfront projects. The OEB/Evel business confederation publicly endorsed the redevelopment in May 2026, adding institutional private-sector weight to what had been a purely governmental narrative.

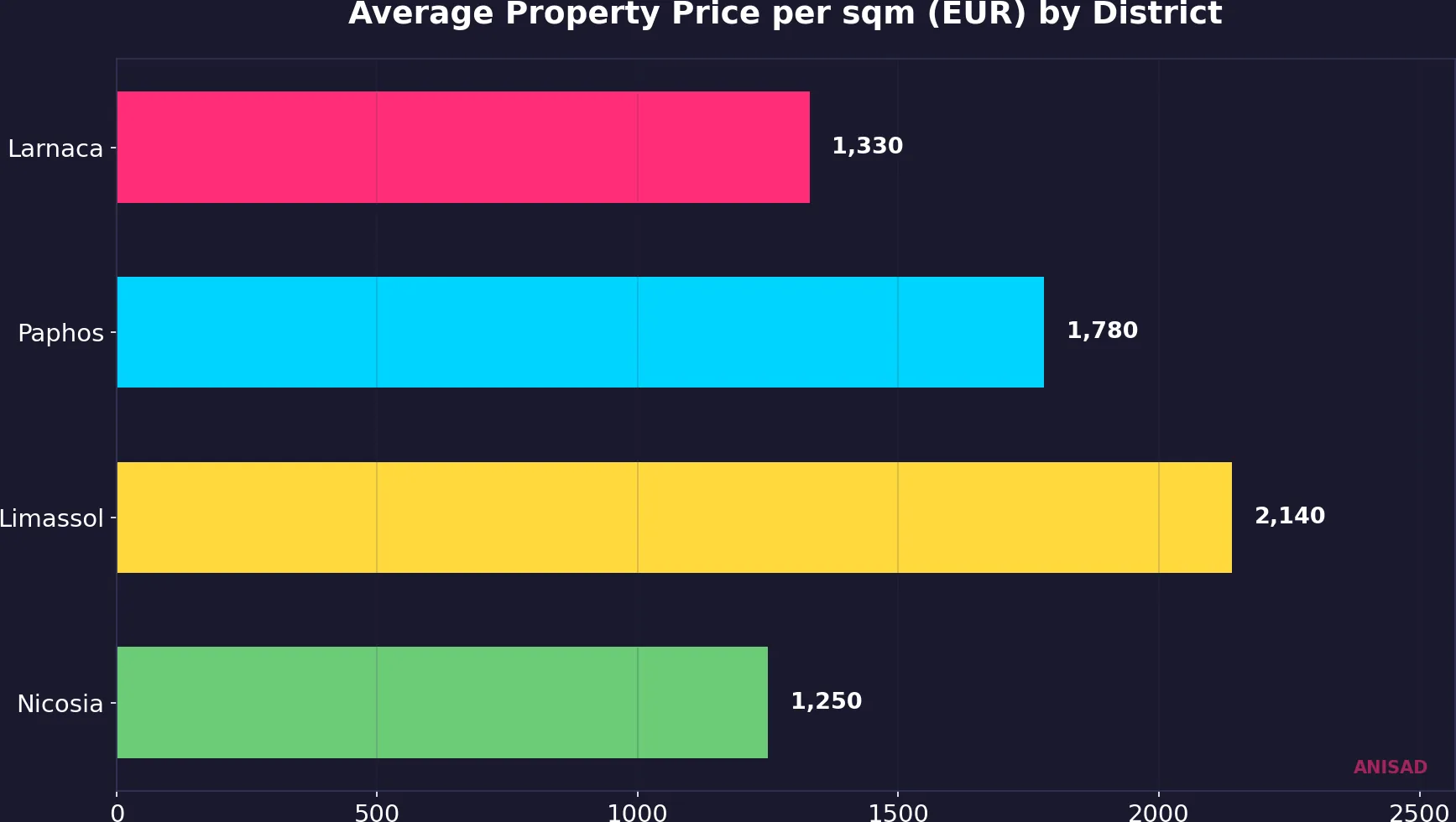

The Price Gap: Larnaca as the Last Affordable Coast

The investment case for Larnaca rests on a simple structural observation: it is the cheapest coastal district in Cyprus, and the gap is not small. Average property prices in Larnaca sit at approximately EUR 1,330 per square metre, compared with EUR 1,780 in Paphos and EUR 2,140 in Limassol. That means Larnaca is more than EUR 800 per square metre cheaper than Paphos and over EUR 800 cheaper still than Limassol — a discount of roughly 38 percent relative to the island's most expensive coastal market.

Yet the market is not standing still. Larnaca apartment prices grew by 11 percent over 2023 and 2024, outperforming the national average before any marina confirmation. This pre-announcement appreciation suggests the market is already pricing in infrastructure expectations — what will happen when a confirmed timeline materialises is the central question for investors.

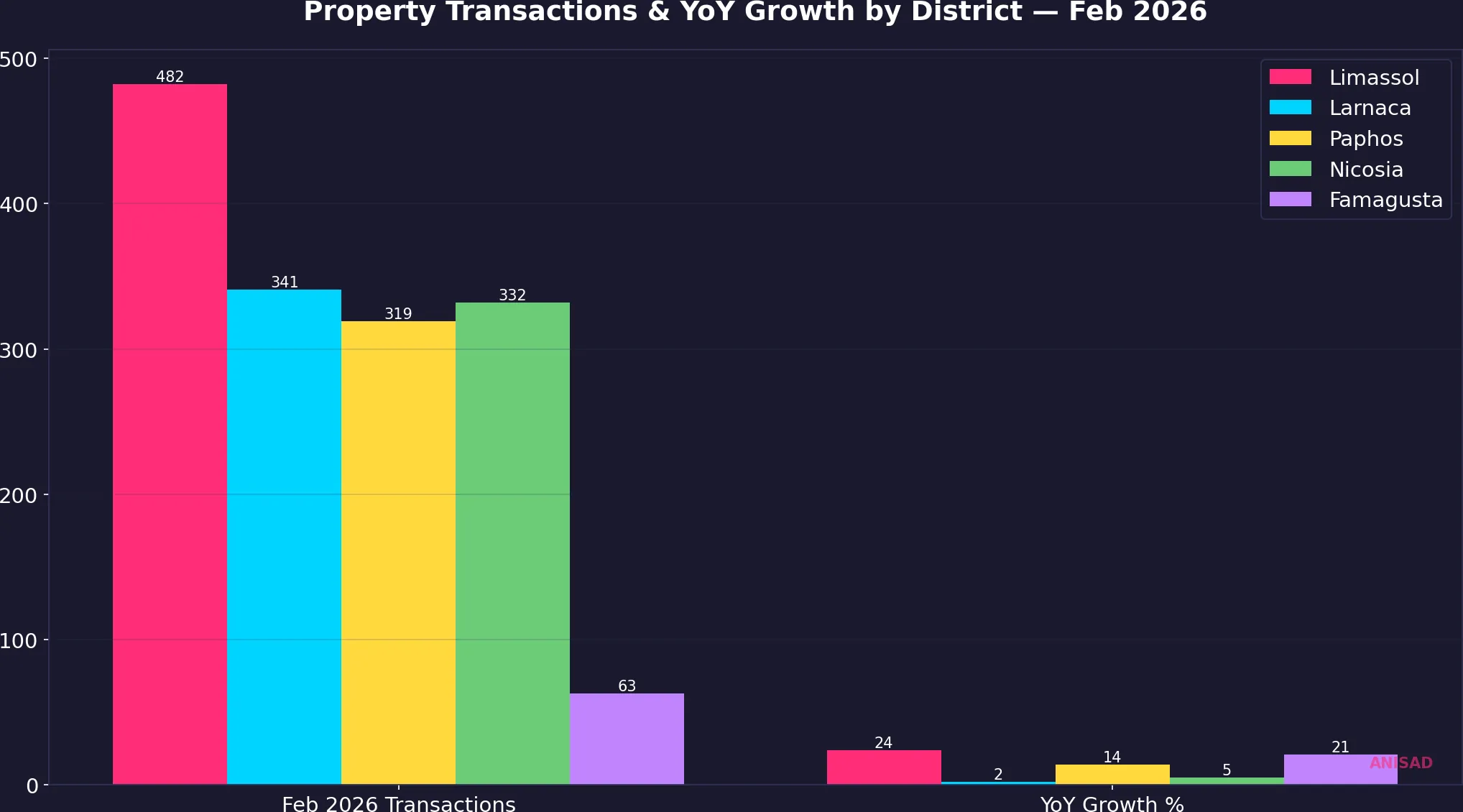

Transaction Activity: Larnaca Lags While Others Surge

February 2026 transaction data from the Department of Lands and Surveys reveals a telling divergence. Cyprus-wide property transactions rose by 12 percent year-on-year to 1,537 properties. Limassol led the charge with a 24 percent increase (482 transactions), followed by Famagusta at 21 percent (63 transactions) and Paphos at 14 percent (319 transactions). Nicosia posted a modest 5 percent gain. Larnaca, however, managed only 2 percent growth — 341 properties, the weakest performance of any district.

This sluggish transaction volume, paradoxically, reinforces the investment thesis rather than undermining it. Larnaca's market is in a holding pattern — buyers sense the infrastructure catalyst but are waiting for confirmed timelines. When the Growthfund financial study delivers its verdict, the pent-up demand is likely to release rapidly. Properties within two kilometres of the development zone are the most exposed to a repricing event, with local market estimates suggesting 15 to 30 percent appreciation within 12 to 18 months of a formal green light.

Mediterranean Context: Where Cyprus Stands

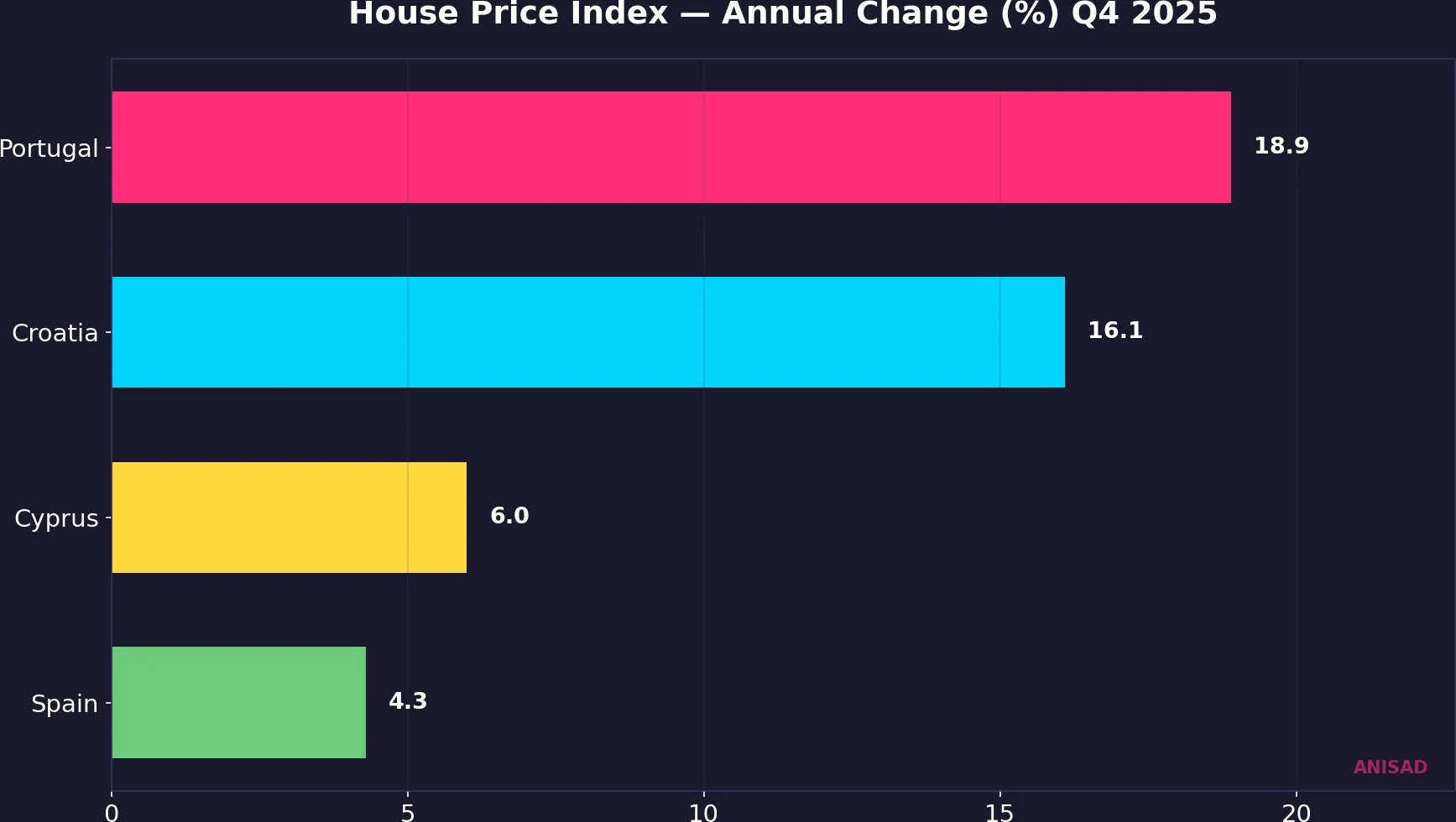

Eurostat's House Price Index for Q4 2025 places Cyprus's annual house price growth at 6.0 percent — moderate compared with Mediterranean peers. Portugal leads at 18.9 percent, Croatia at 16.1 percent, while Spain posts 4.3 percent. Cyprus sits in the middle band: not overheating nationally, but with significant district-level variation. The national figure masks sharp divergence — Limassol and Paphos drive most of the growth, while Larnaca's lower trajectory keeps the island average in check.

This context matters because it reveals what infrastructure-led repricing looks like in peer markets. Portugal's nearly 19 percent growth has been driven partly by Golden Visa demand and infrastructure investment along the Algarve; Croatia's surge followed EU accession and coastal tourism infrastructure upgrades. Cyprus's more measured pace suggests there is room for a district-specific acceleration — particularly if a confirmed marina timeline converts Larnaca from a value play into a premium destination.

Who Stands to Gain — and Who Should Worry

The clearest beneficiaries are developers with existing land banks near the marina zone. They have acquired at Larnaca's historically discounted prices and stand to benefit from a structural repricing. Hotel and hospitality operators eyeing marina-adjacent sites gain a decade-long visibility window thanks to the 2035 national strategy. Foreign investors looking for the next value play after Paphos — where prices have already risen sharply — now have a policy-backed thesis for Larnaca.

The cautious investor should weigh the risks carefully. Political risk is elevated with parliamentary elections approaching — the project could stall during government transition. The separated development model, while more pragmatic, is untested for this specific site and may encounter financing challenges without a single anchor investor. And the track record speaks for itself: three failures in twenty years mean a fourth termination would devastate investor confidence in Larnaca for a generation.

What to Watch: A Reader Playbook

For investors and market watchers, several leading indicators will signal whether the marina thesis is materialising or stalling:

- Growthfund financial study release — the single most important milestone. A positive verdict with clear financing terms converts speculation into a defined project timeline.

- Building permit activity in the Larnaca district — a surge in permits for marina-adjacent plots would confirm developer conviction.

- Transaction volume acceleration — if Larnaca's 2 percent growth rate jumps to double digits, the market is pricing in confirmation.

- Government procurement timeline — an official tender announcement with defined phases and deadlines.

- Parliamentary election outcomes — any shift in government priorities toward the marina project.

The thesis would weaken if the financial study is delayed beyond Q3 2026, if the separated model fails to attract qualified bidders, or if political transition freezes the procurement process. Investors should set a personal deadline: if no tender is issued by end of 2026, the project may be entering another multi-year limbo.

The Structural Opportunity

The Larnaca marina is not just another waterfront development — it is a test of whether Cyprus can execute large-scale infrastructure outside the Limassol corridor. At EUR 1,330 per square metre, Larnaca offers the widest price gap versus any other coastal district. The government's 2035 luxury yachting strategy, business federation endorsement, and the pragmatic separation of port and marina operations represent the strongest institutional alignment this project has ever had. The risk is real — twenty years of failure commands respect. But for the first time, the approach has changed rather than just the contractor. That is the signal worth paying attention to.

Data sources: Department of Lands and Surveys (DLS) — property transaction data, CYSTAT — House Price Index, Eurostat prc_hpi_q — EU harmonised house price indices, Cyprus Mail — Growthfund study coverage, Cyprus Property News — marina development updates, OEB/Evel — business federation endorsement, Deputy Ministry of Tourism — 2035 yachting strategy, Landbank Analytics — district-level property analytics