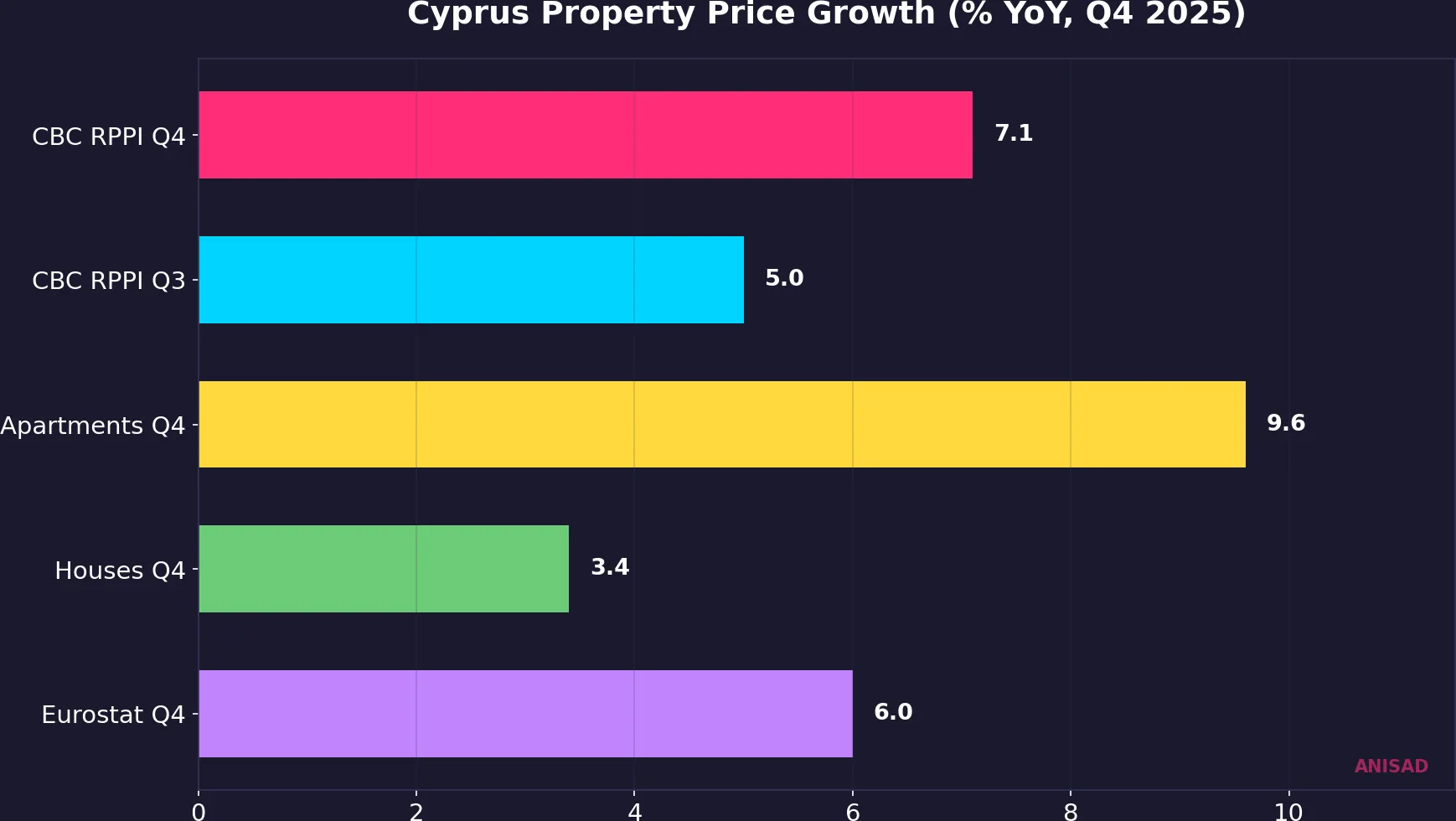

Cyprus property prices have officially surpassed their 2008 pre-crisis peak, marking a watershed moment in the island's real estate recovery. The Central Bank of Cyprus reports that its Residential Property Price Index (RPPI) accelerated to 7.1% year-on-year growth in Q4 2025, up from 5.0% in Q3, with the apartment segment surging at 9.6% annually. This is not a gentle return to old highs - it is a sharp re-acceleration that redefines the market's trajectory and raises urgent questions about sustainability.

The Numbers Behind the Milestone

The acceleration in Q4 2025 was broad-based but uneven. The Central Bank of Cyprus RPPI, which tracks actual transaction prices, recorded a quarterly gain of 2.3% - double the 1.2% registered in Q3. This quarterly doubling is a clear sign that price momentum is building, not fading. Apartments led the charge at 9.6% annual growth, while houses grew a more modest 3.4%.

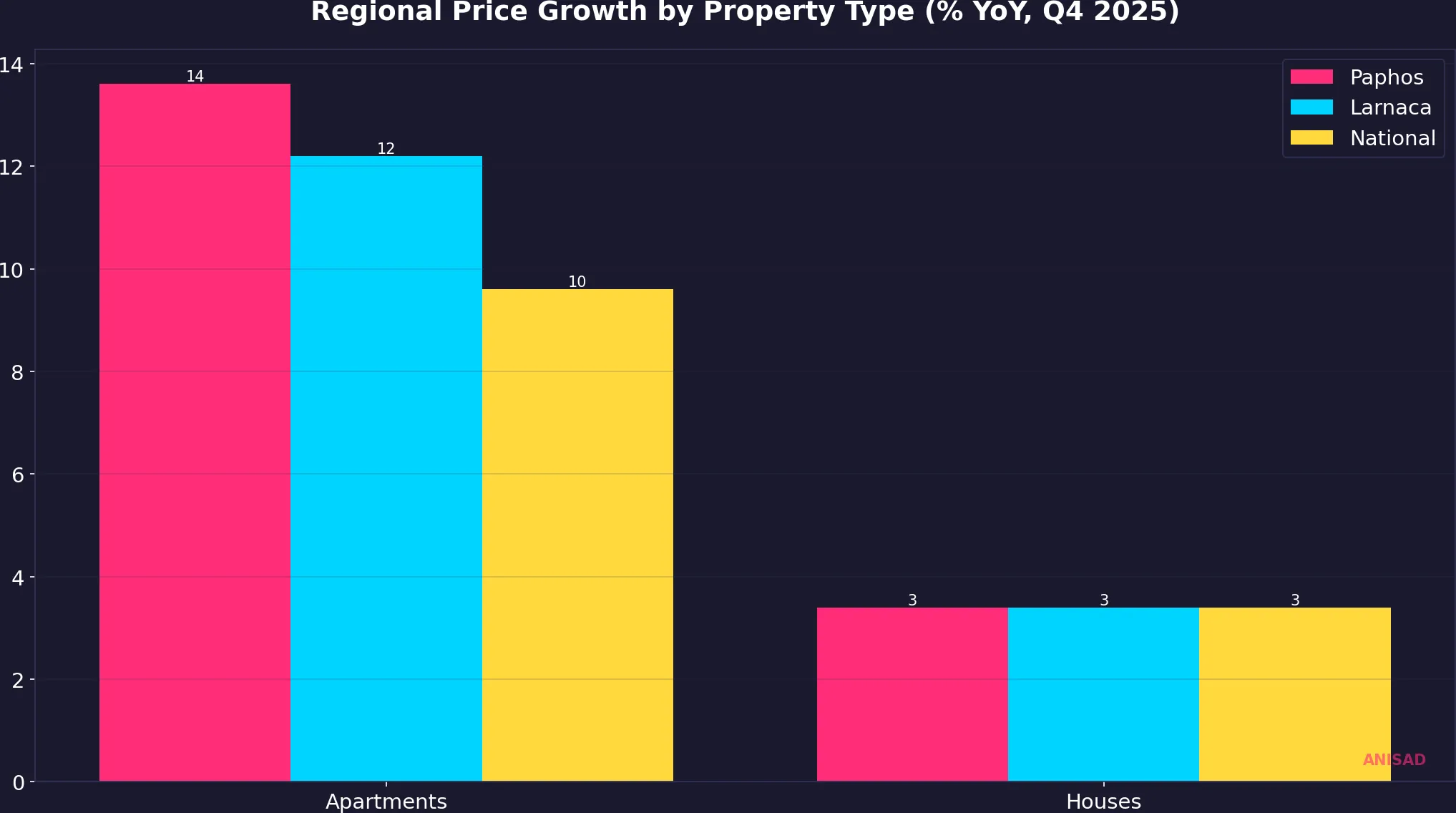

Regional disparities paint an even more dramatic picture. Paphos apartment prices surged 13.6% year-on-year, and Larnaca apartments climbed 12.2% - both approaching the double-digit territory that historically precedes either a supply response or a correction. Limassol, the traditional price leader, is no longer the fastest-growing district - a geographic rebalancing that suggests capital is actively seeking value in underpriced coastal markets.

Two Indices, Two Stories

Perhaps the most significant analytical finding is the divergence between the two official price measures. The Central Bank's transaction-based RPPI shows accelerating growth at 7.1% year-on-year, while CYSTAT's assessment-based House Price Index reports a more muted 6.0% annual increase for the same quarter (Eurostat data). Earlier in 2025, the CYSTAT HPI even dipped to near-zero quarterly growth before recovering, while the CBC RPPI never showed such weakness.

This divergence is not a statistical curiosity - it signals a bifurcated market. The transaction-based index captures what buyers are actually paying, heavily influenced by foreign purchasers competing for prime coastal apartments. The assessment-based index reflects broader market valuations that include properties not actively traded. When transaction prices accelerate faster than assessed values, it typically means a specific buyer segment is bidding up prices in targeted sub-markets while the broader housing stock appreciates more slowly.

Foreign Buyers as the Primary Catalyst

Foreign buyer transactions rose 23.9% year-on-year in Q4 2025, with non-domestic purchasers now accounting for approximately 49% of all property transactions. By January 2026, the foreign share surged further to 30.8% month-on-month growth. This demand is structural, not speculative: Cyprus offers EU residency through property investment, a favourable tax regime, and English-language legal infrastructure - advantages that have only grown as competing Golden Visa programmes in Portugal, Greece, and Spain face restrictions or outright bans.

The credit side supports this narrative. Net mortgage lending expanded 23.1% to EUR 1.338 billion in 2025, while the average mortgage rate stood at 3.12% in December 2025 - competitive by European standards and well below the levels that would typically trigger affordability stress. Building permits surged 36.1% to 14,401 units in January-November 2025, indicating that the supply side is responding, though with the typical 18-24 month lag before new units reach the market.

The Two-Speed Market Emerges

Landbank Analytics' 2025 data reveals a structural split. Apartments dominated the affordable segment with 6,382 transactions worth EUR 1.77 billion, with 74% of sales priced below EUR 300,000. Houses told a different story: only 1,437 transactions, with 40% in the EUR 300,000-500,000 bracket. Remarkably, just seven houses sold below EUR 150,000 across all of Cyprus in 2025 - effectively eliminating the entry-level detached housing option.

This bifurcation has consequences. The apartment segment is absorbing almost all first-time buyer and investor demand, creating a concentration risk where price pressure is focused on a narrowing pool of product types. For domestic buyers, the practical message is stark: affordable homeownership in Cyprus increasingly means an apartment, not a house.

How Cyprus Compares: Mediterranean Context

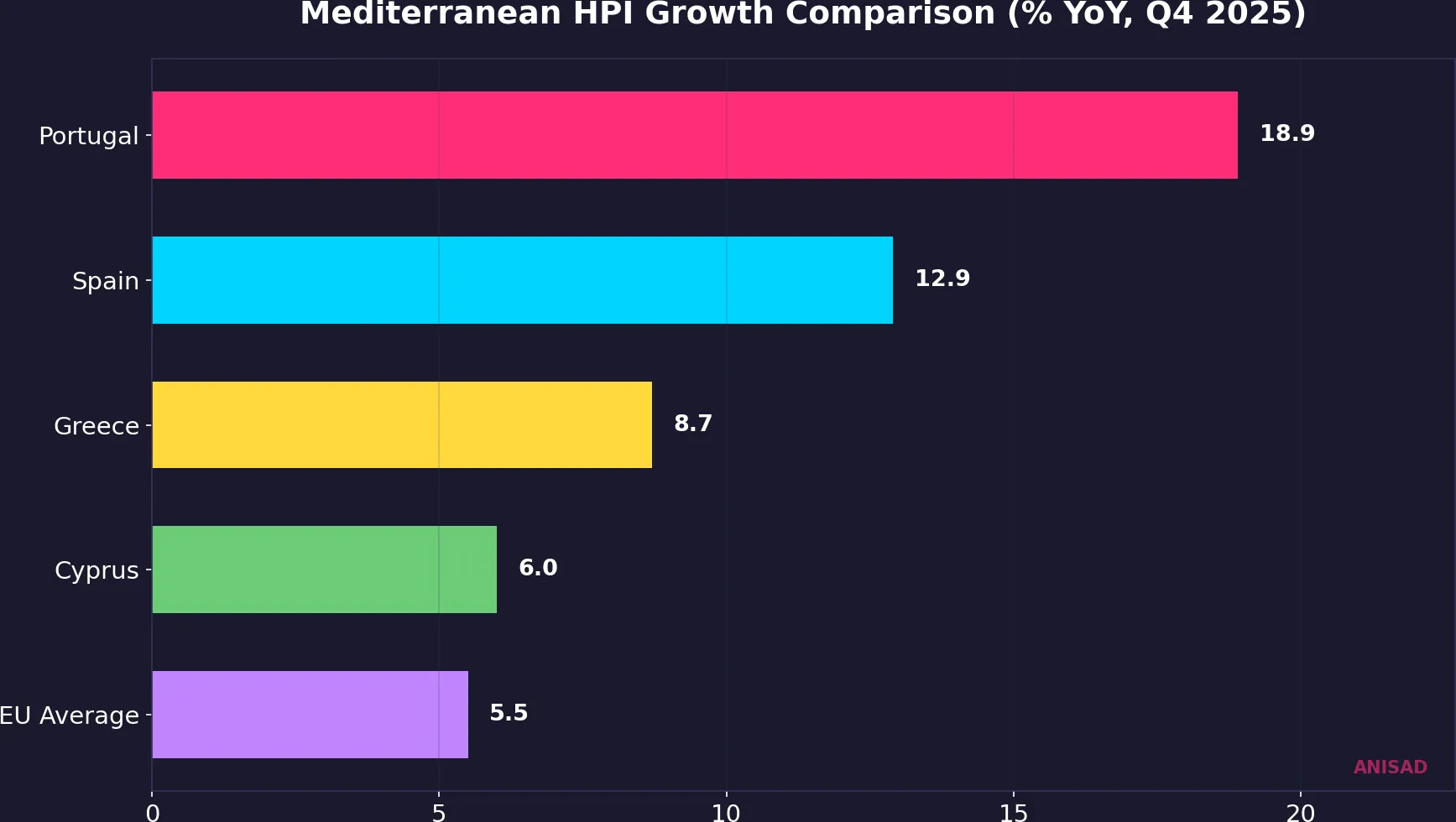

Despite the accelerating headline numbers, Cyprus remains the slowest-growing major Mediterranean market in Eurostat's Q4 2025 data. Portugal led at 18.9% year-on-year, Spain recorded 12.9%, and even Greece outpaced Cyprus. The EU average stood at 5.5%, meaning Cyprus at 6.0% (Eurostat measure) is above average but far from the overheating seen in Iberian markets.

This relative positioning matters. Spain's recent political backlash against foreign buyers - with proposed restrictions and increased taxes - could redirect capital towards Cyprus, which still offers a relatively welcoming regulatory environment. Portugal's near-20% price growth is widely viewed as unsustainable, and any correction there would further establish Cyprus as a safer alternative for Mediterranean property investors seeking EU exposure without peak-cycle risk.

What Makes This Different from 2008

The 2008 crisis in Cyprus was driven by speculative lending, overleveraged domestic buyers, and a banking sector that collapsed under the weight of Greek sovereign debt exposure. Today's market fundamentals are materially different. Foreign cash buyers constitute a significant share of transactions, reducing systemic banking risk. Mortgage rates are controlled and competitive at 3.12%. The construction permit surge suggests a supply response is in motion, unlike the pre-crisis period where land banking dominated.

However, passing the pre-crisis nominal peak does not mean the market is risk-free. The apartment segment's 9.6% annual growth rate, concentrated in coastal districts, mirrors the kind of asset-class-specific overheating that preceded corrections in other markets. The question is whether the supply pipeline of 14,401 permitted units can absorb demand before prices detach further from domestic earning power.

What to Watch: A Reader Playbook

For investors and market observers monitoring this cycle, several leading indicators will determine whether the current acceleration is the beginning of sustained growth or the final push before a plateau.

- Index divergence: if the gap between CBC RPPI (transaction) and CYSTAT HPI (assessment) continues to widen, it signals that foreign-driven transactions are increasingly disconnected from the broader market. Narrowing would suggest genuine broad-based appreciation.

- Foreign buyer share: crossing 50% of transactions would represent a structural dependency that makes the market vulnerable to external policy shocks.

- Completion-to-permit ratio: the 14,401 building permits issued need to translate into completed units within 18-24 months. If completions lag significantly, supply will remain constrained and prices will continue to rise.

- Mortgage rate trajectory: any move above 4% would test affordability for domestic buyers and shift demand composition further toward cash-heavy foreign purchases.

- Paphos and Larnaca trajectory: these districts, now growing at 13.6% and 12.2% respectively, are the bellwethers of geographic rebalancing.

The Industry's Own Signal

Perhaps the most telling qualitative signal came from CPDA chairman Yiannis Misirlis, who publicly declared in April 2026 that the sector is entering a "period of structural transformation." When an industry lobby group shifts its messaging from growth to adaptation, it typically signals that insiders expect the easy gains to moderate. Whether this translates into policy advocacy, supply acceleration, or simply rhetorical repositioning will become clear in the coming quarters.

Conclusion

Cyprus property prices have passed their 2008 peak, but this market bears little resemblance to the one that crashed. Foreign demand, competitive lending rates, and a genuine supply response distinguish the current cycle from pre-crisis excess. The risk is not a 2008-style collapse but rather a bifurcation - a market where foreign-driven coastal apartments accelerate beyond domestic reach while the broader housing stock follows a different, slower trajectory. The next twelve months will reveal whether the supply pipeline can close the gap before affordability becomes the political crisis it already is in much of Southern Europe.

Data sources: Central Bank of Cyprus RPPI Q4 2025, CYSTAT House Price Index Q4 2025, Eurostat House Price Index (prc_hpi_q) Q4 2025, Department of Lands and Surveys transaction data, Landbank Analytics 2025 Market Report, CYSTAT building permits data (Jan-Nov 2025)