Mediterranean property markets are entering a new phase: the residency incentive era is fading, but cross-border capital has not left the region. Portugal still drew €3.905 billion into real estate in 2025, Spain still closed the year with 752,098 total transactions, and Greece still expanded its investor base to 28,589 active Golden Visa permits. The core change is not demand destruction. It is demand sorting.

The New Baseline: Capital Is Repricing Regulatory Friction, Not Exiting the Region

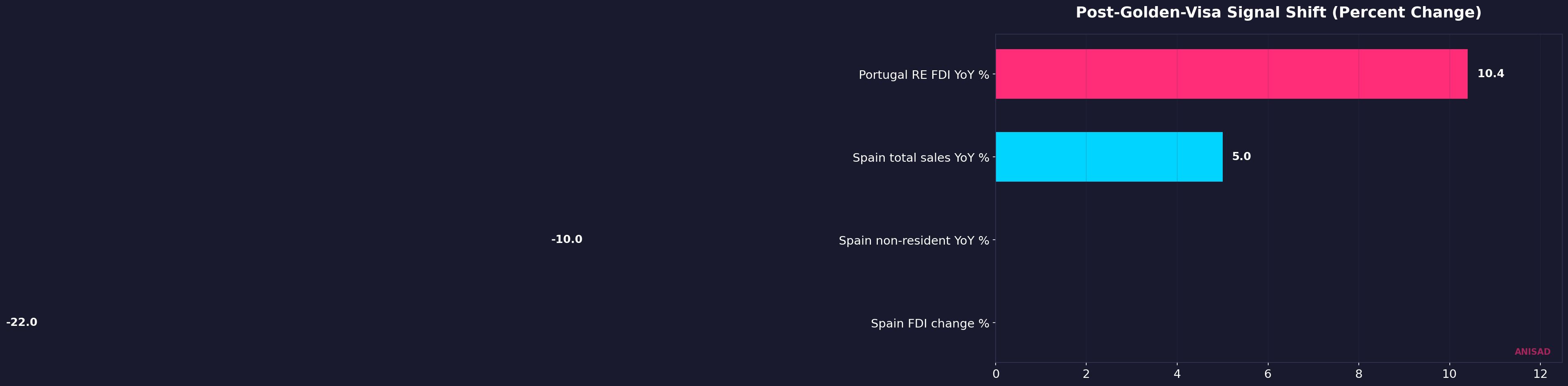

For years, the strategic assumption in Mediterranean policy circles was straightforward: if you reduce or remove residency-by-real-estate incentives, foreign property demand should cool quickly. The latest data breaks that assumption. In Portugal, direct real-estate Golden Visa access was removed, yet real-estate FDI climbed to approximately €3.905 billion and represented roughly 46.0% of total FDI. That composition is not evidence of disappearing capital. It is evidence that investors are separating residency mechanics from asset exposure.

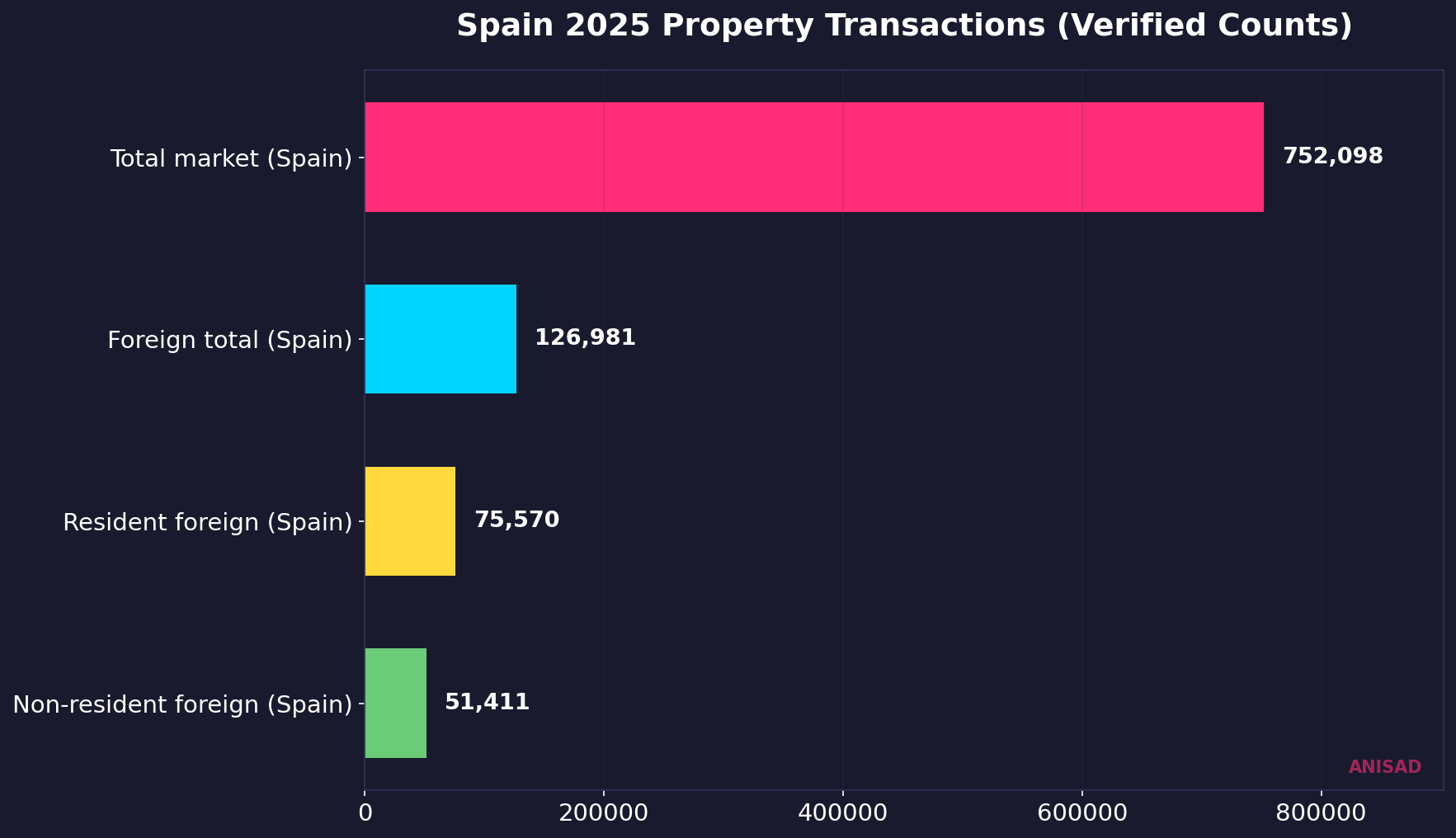

Spain provides the second leg of the same argument. Non-resident foreign buyer activity dropped around 10% year-on-year to 51,411 transactions, but the aggregate market still reached 752,098 sales. Resident foreign demand rose to 75,570, keeping overall foreign participation meaningful. In other words, one buyer cohort slowed, but the market architecture remained active. This is exactly what mature international markets do under policy stress: they rebalance participant mix before they reprice fundamentals.

Threshold Competition Is Now a Strategic Positioning Game

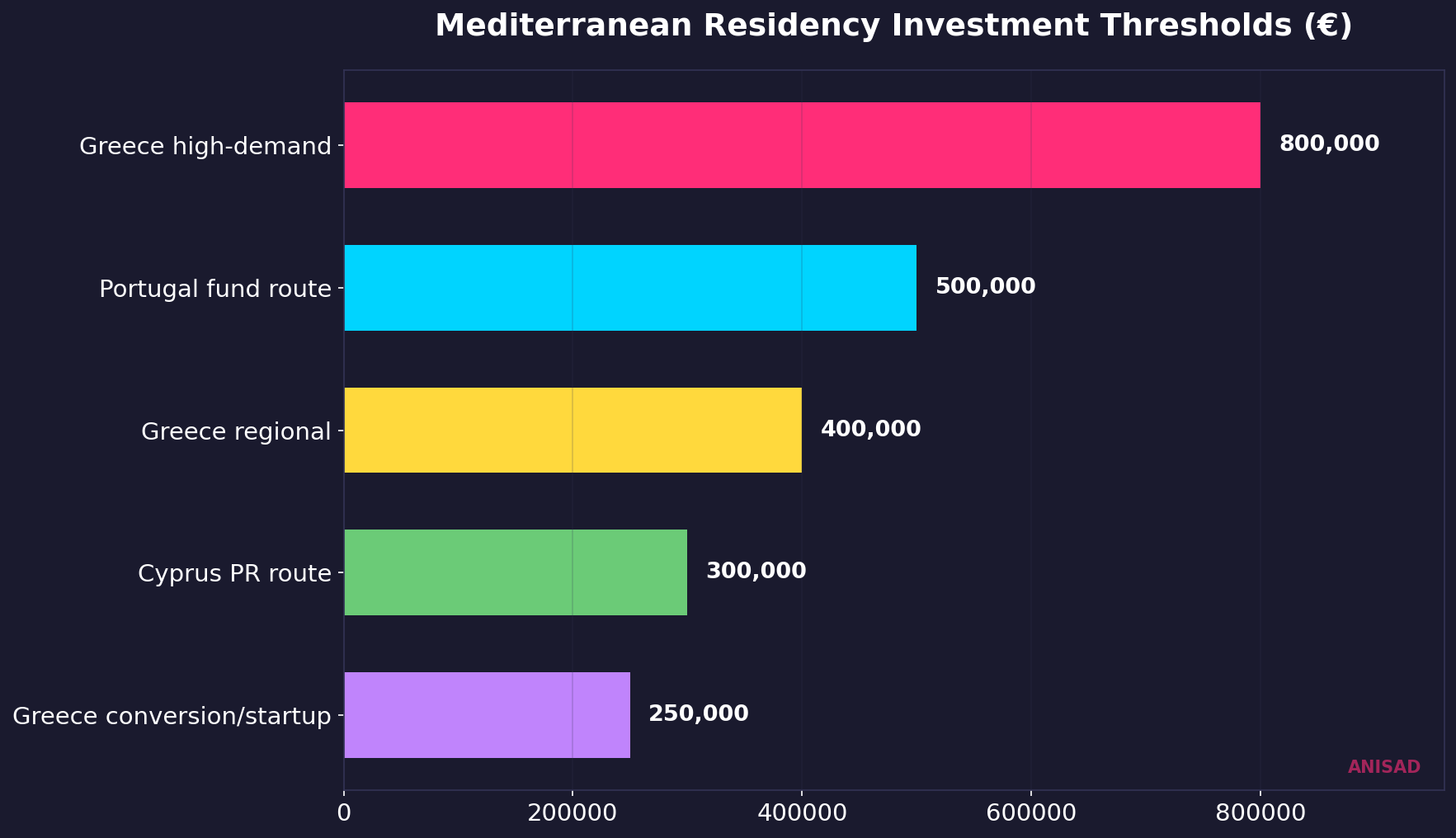

The post-Golden-Visa landscape is no longer binary (open vs closed). It is tiered. Greece now operates with multiple threshold bands up to €800,000 in high-demand zones, while preserving lower pathways for specific conversion and startup routes. Portugal shifted investor pathways toward higher-ticket fund structures. Cyprus remains relatively accessible on headline threshold, but faces domestic debate over tighter purchase controls for non-EU buyers. Investors are reading this as a portfolio construction problem: where can capital still enter, under what structure, with what future policy risk?

That creates a critical strategic distinction for governments. A low threshold alone is no longer sufficient to win durable inflows. Predictable rulemaking, execution speed in permitting, and legal clarity around ownership and rental income treatment increasingly determine whether capital is patient or tactical. In this cycle, jurisdictions that signal policy volatility may still attract one-off buyers, but they struggle to retain institutional conviction.

Signal Quality: Why the Same Region Shows Both Growth and Flight

The contradictory headlines across the Mediterranean are real, and they can coexist. Portugal can show double-digit real-estate FDI growth while affordability worsens. Spain can print robust transaction volume while non-resident buyers and broader FDI weaken. Greece can expand active permits while simultaneously forcing rental formalization and reshaping landlord incentives. These are not data errors. They are symptoms of a transition from policy-arbitrage capital to strategy-driven capital allocation.

For allocators, this means headline growth rates are no longer enough. The key filter is now durability of demand under tightening conditions. Which markets maintain volume after regulatory shocks? Which buyer cohorts are replacing those that exit? Which governments are pairing demand controls with supply-side delivery? Without that second layer, investors risk confusing cyclical resilience with structural strength.

Stakeholder Impact: Who Wins and Who Faces Compression

- Governments with coherent, staged regulation win by attracting higher-quality, longer-duration capital.

- Institutional investors win where legal clarity lowers compliance and execution risk.

- Developers with adaptive product mix win as buyer profiles shift from residency-led to lifestyle-plus-yield demand.

- Local first-time buyers remain pressured where supply remains slow and construction lags demand.

- Markets relying on one foreign cohort lose bargaining power when nationality mix rotates quickly.

What to Watch in the Next 6-24 Months

Three forward indicators should anchor decision-making. First, monitor foreign-buyer composition, not only total volume. A stable aggregate can hide significant risk transfer between cohorts. Second, track supply conversion speed: permits, completions, and rental-stock formalization. Without these, price pressure persists regardless of demand-side controls. Third, evaluate policy sequencing discipline. Sudden, politically timed restrictions tend to raise risk premia more than they improve affordability.

For Cyprus specifically, the strategic window is narrow but meaningful. The country can absorb reallocated Mediterranean capital if it preserves regulatory credibility while improving supply responsiveness and transaction transparency. If policy debate drifts into abrupt or inconsistent implementation, that same capital can reroute quickly to alternative jurisdictions. In a post-Golden-Visa era, capital is still available. Trust is the scarce asset.

Conclusion

The Mediterranean investment story did not end with Golden Visa retrenchment. It matured. The next winners will be markets that combine openness with enforceable rules, discipline with speed, and growth narratives with measurable supply execution. Capital is no longer paying for residency shortcuts. It is paying for policy quality.

Data sources: Bank of Portugal FDI reporting (2025), Spanish Housing Ministry transaction data (2025), Spanish Property Insight market analyses (2026), Greek government Golden Visa and rental policy updates (2026), Kathimerini Cyprus reporting on Mediterranean residency positioning (2026), Euronews Business reporting on Spain FDI trend (2026), Eurostat / CYSTAT HPI indicators (Q3 2025)