European real estate in 2026 has been repriced less by classic supply-and-demand mechanics and more by geopolitical transmission channels. The Iran war shock hit mortgage expectations, energy costs, construction inputs, and tourism confidence almost simultaneously. Then, a sudden ceasefire and a sharp oil pullback interrupted that trajectory without fully undoing the damage already priced into credit and investment behavior.

The first-order shock: rates, confidence, and deal flow

The UK housing complex offered the clearest high-frequency stress signal. RICS buyer enquiries moved deeper into contraction at -26 (from -15 a month earlier), while two-year and five-year fixed mortgages climbed to 4.93% and 5.03% respectively. On one repricing day, lenders pulled 330 mortgage products. These are not abstract volatility markers; they are immediate constraints on affordability and transaction velocity across mortgage-led markets.

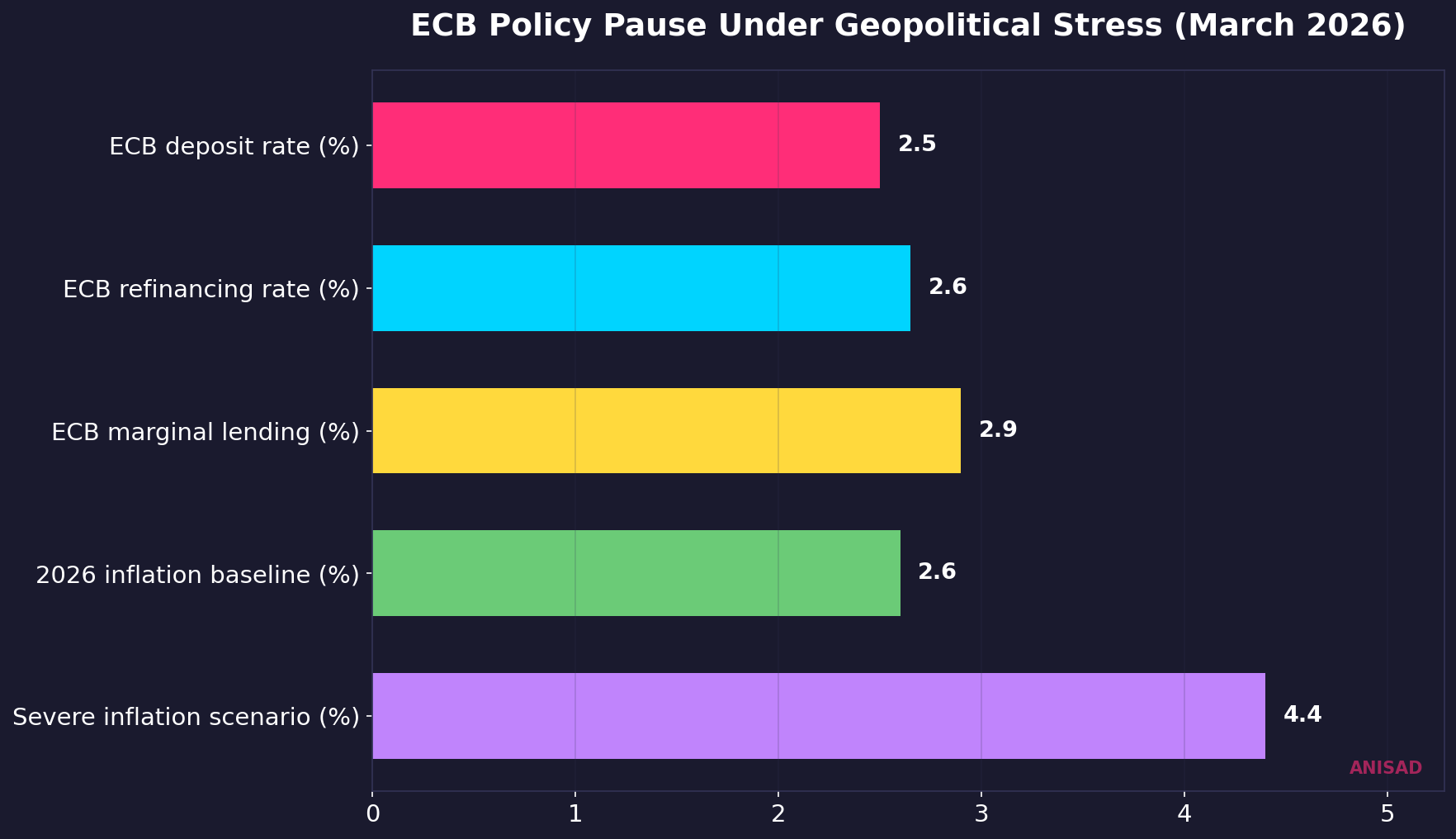

For continental Europe, the policy anchor also shifted. On 19 March, the ECB kept rates unchanged at 2.50% (deposit), 2.65% (main refinancing), and 2.90% (marginal lending), ending a six-cut easing sequence. At the same time, inflation expectations were revised to 2.6% in baseline and 4.4% in severe scenarios, with growth guidance around 0.9%. In practical property terms, this changes financing assumptions used by developers, lenders, and acquisition committees.

Cyprus as a transmission case study, not an exception

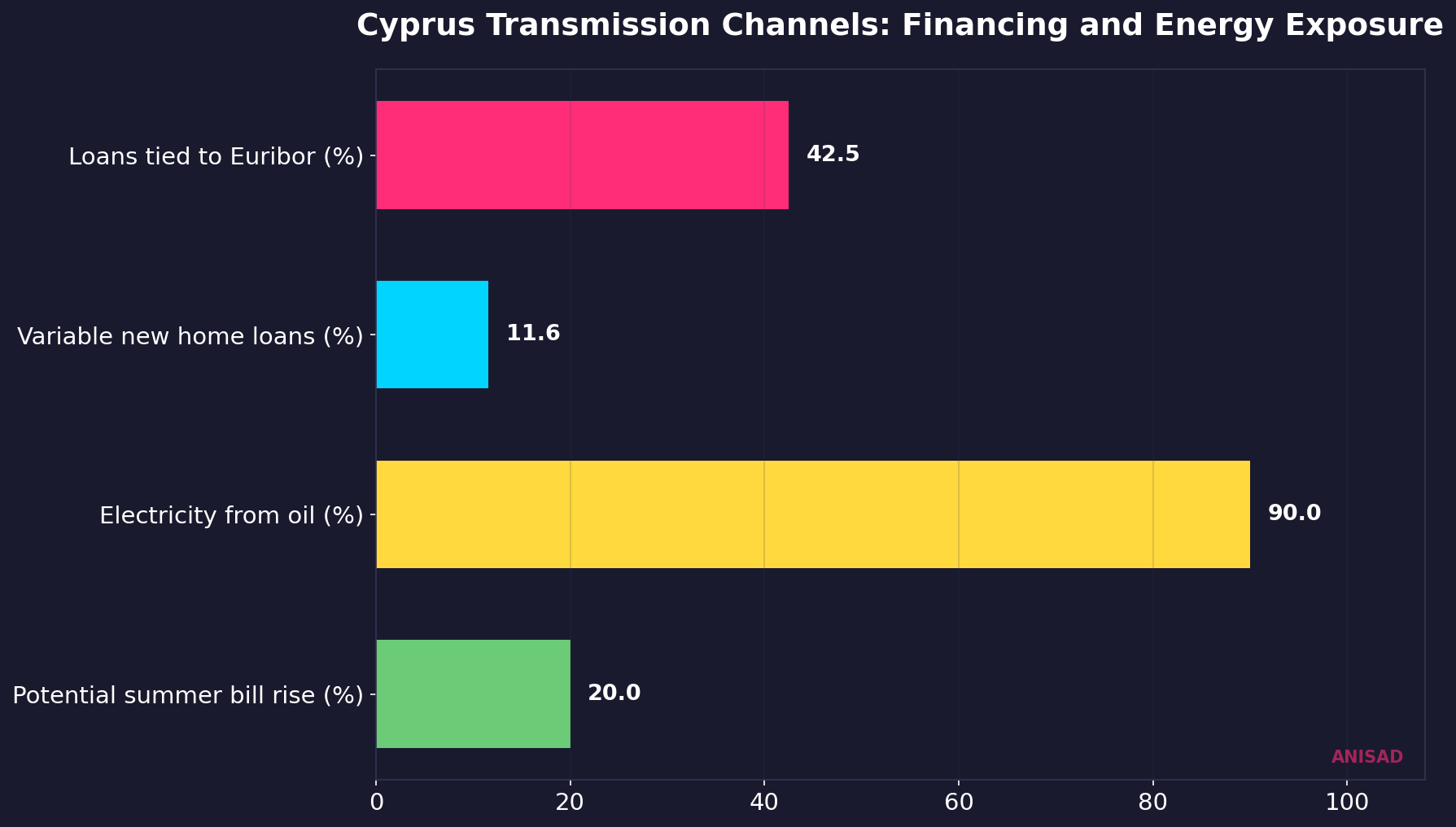

Cyprus illustrates how geopolitical shocks move through a smaller open property market. Around 40-45% of loans are linked to Euribor benchmarks, and Euribor itself rose 20 bps in about 20 days during the conflict phase. Borrowers hitting reset windows experienced higher payments immediately, while new buyers faced a stricter affordability envelope despite no formal ECB hike in that period.

The energy channel is equally direct. Cyprus still generates roughly 90% of electricity from petroleum products. As Brent moved into stress territory, utility operators signaled likely household electricity increases of 5-7% by May, potentially up to 20% by August under sustained high oil assumptions. That cost pass-through affects not only household budgets but also construction, refurbishment, and operating expenditure assumptions used in yield underwriting.

Tourism-confidence linkage and second-order property effects

In Cyprus, tourism stress added a separate demand-side risk. Operators reported cancellation clusters including 13 guest cancellations and 50 room nights in one week, with an estimated 35% revenue hit in one observed short-term rental operation. This matters to real estate because tourism is often the top-of-funnel for relocation, holiday-home acquisition, and short-let investment demand. A war-adjacent risk perception shock can compress that funnel before it appears in official transfer data.

At the European scale, the Commission warned that energy normalization may lag even if hostilities cool, citing roughly +70% gas and +60% oil moves during the acute phase and an estimated €14 billion additional fossil-fuel bill. That framing is important: it implies lingering cost pressure in building operations and materials, which can keep cap rates and development hurdle rates elevated longer than headline ceasefire news would suggest.

Ceasefire relief: meaningful, but not a full reset

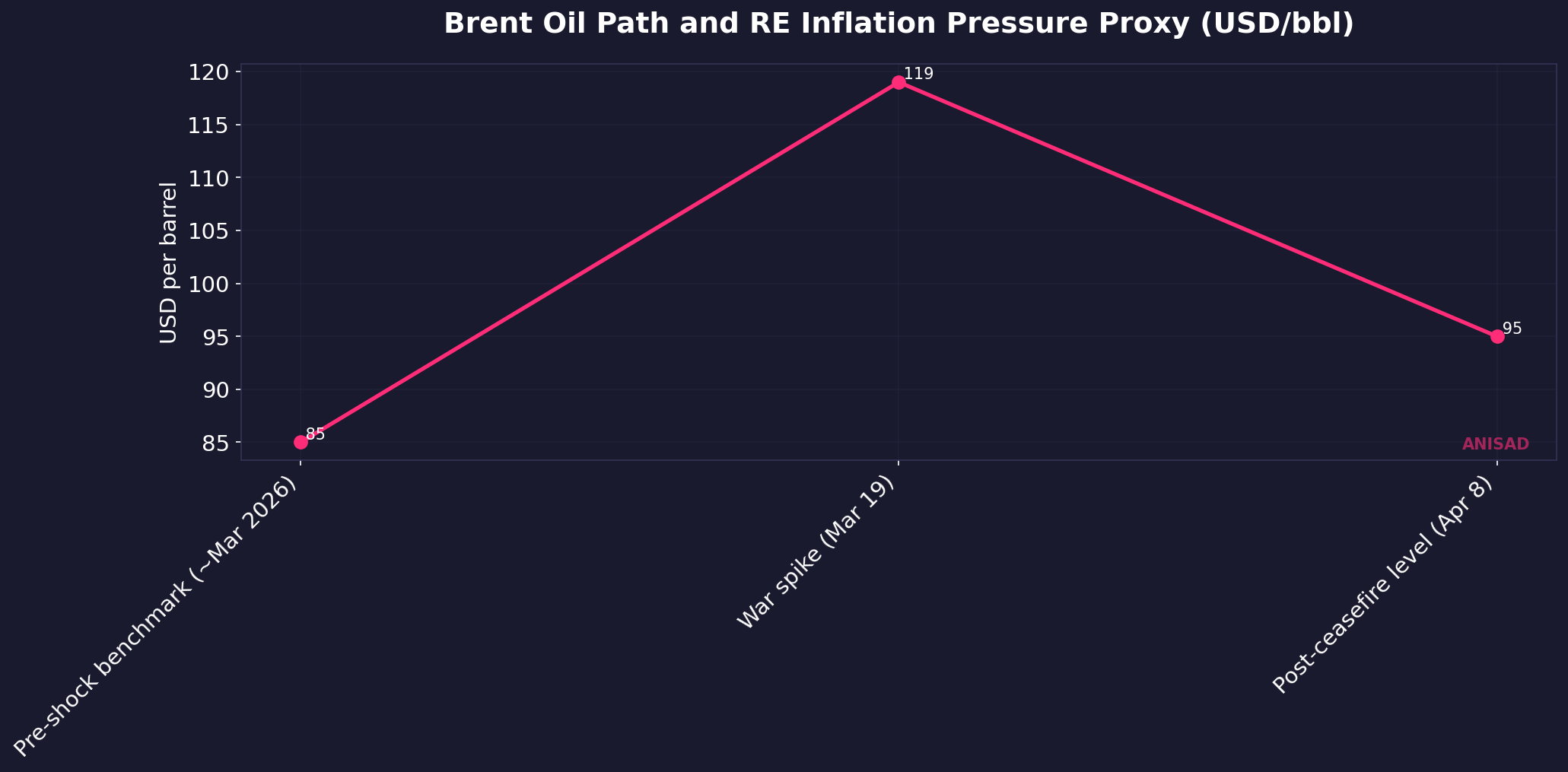

The April ceasefire headline changed near-term inflation optics quickly. Brent retraced sharply, falling from war-spike levels toward the mid-90s, at one point reflecting a roughly 16% drop below the $100 threshold. This is a genuine macro relief input for real estate: lower fuel pressure can soften expected policy restrictiveness, support logistics and construction margins, and improve visibility for debt pricing.

Still, ceasefire is not equivalent to structural normalization. Lenders and developers typically re-risk slower than markets re-price headlines. In the UK, large housebuilder behavior (including land-acquisition freezes) indicates that board-level capital allocation has already shifted to a defensive posture. In Spain, emergency rental interventions introduced under conflict justification (including a 2% rent cap regime and forced extension mechanisms) reinforce the regulatory-risk premium that institutional capital now has to model explicitly.

Who gains, who loses, and what to watch through 2026

- Likely beneficiaries: cash buyers, low-leverage allocators, owners of energy-efficient stock, and markets with stable policy regimes.

- Most exposed: variable-rate households, leverage-dependent developers, tourism-sensitive rental operators, and jurisdictions with intervention-heavy rental policy drift.

- Key watchpoints: Euribor direction vs ECB guidance, energy pass-through into utilities and materials, summer tourism booking recovery, and developer land-acquisition behavior in the UK and Southern Europe.

The central investment conclusion is not that the shock has passed, nor that a deep crisis is guaranteed. It is that European RE now trades on a wider geopolitical-risk distribution. For Cyprus and Mediterranean markets, the next phase will be determined by whether lower oil sustains long enough to re-open mortgage momentum and tourism confidence before higher-for-longer financing assumptions become entrenched in transaction pricing.

The 2026 market is no longer pricing just rates and supply. It is pricing geopolitical transmission speed.

Data sources: Estate Agent Today (RICS demand and UK mortgage repricing, March 2026), Kathimerini Cyprus (Euribor transmission to Cyprus loans, March 2026), European Central Bank press communication (policy rates and inflation scenarios, 19 March 2026), Cyprus Mail and inbusinessnews (Cyprus electricity cost pass-through, March 2026), Kathimerini Cyprus business (tourism cancellation effects in Cyprus, March 2026), Euronews business and EU Energy Commissioner statement (EU energy-cost persistence, April 2026), inbusinessnews/Reporter (Brent move after US-Iran ceasefire, April 2026), Spanish Property Insight (RDL 8/2026 rental interventions in Spain), The Guardian business (Berkeley Group defensive land strategy, April 2026)