Cyprus is approaching a decisive policy moment in real estate. Parliament has advanced a bill that would tighten how non-EU nationals buy land and residential assets, while demand from foreign buyers is still running hot. That combination matters: when restrictions arrive during a strong cycle, market impact is rarely linear. The question is not only whether prices go up or down. The bigger question is who gets priced in, who gets priced out, and which districts absorb the policy shock first.

What Is Actually Being Proposed

Recent committee-stage drafts, now moving toward plenary vote, converge around a stricter regime for foreign ownership of sensitive land categories. The reported package includes a ban on foreign purchases of agricultural and forest land, a one-unit residential cap for non-EU nationals, and constraints around strategic zones such as ports, airports, military facilities, beaches, and the Green Line. Some drafts also include longer residency/retention requirements and stronger beneficial-ownership disclosure obligations.

From a market-design perspective, this is a targeted intervention rather than a total freeze. The intent appears to be containment: preserve strategic and undeveloped land, reduce regulatory arbitrage via foreign-controlled entities, and redirect external capital toward lower-risk, already-developed inventory. That differs from blunt anti-foreign rhetoric seen in some other jurisdictions. It also means the effect will depend heavily on asset class and geography.

Demand Pressure Before Implementation

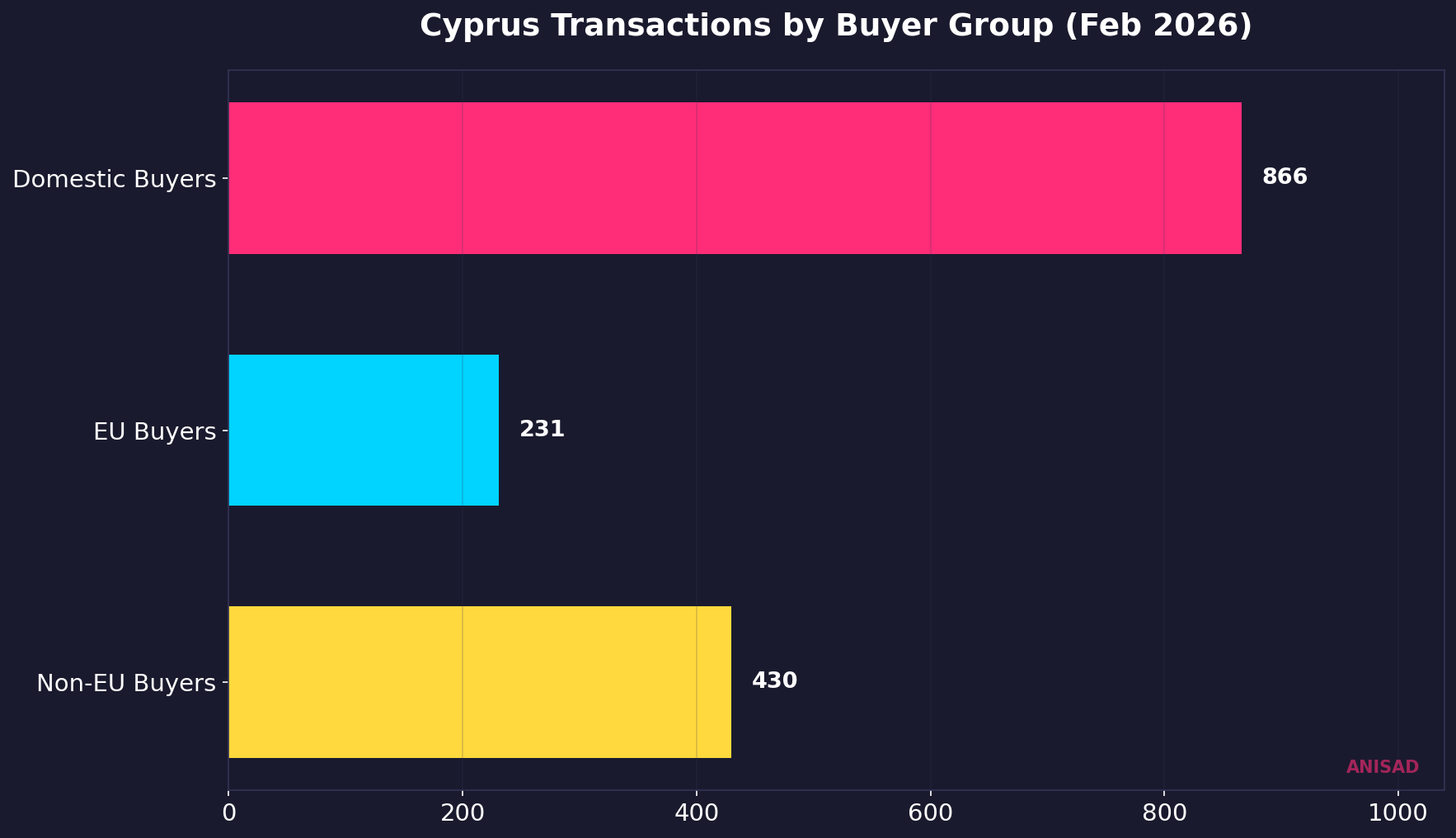

Cyprus entered this policy window with powerful transaction momentum. Public market reporting for February 2026 shows 1,537 contracts, up 11% year-on-year and close to historical monthly highs. The composition of buyers is the key signal: non-EU buyers reached 430 transactions in the month, EU buyers 231, while domestic buyers accounted for 866. In practice, that means foreign capital is no longer marginal in price formation, especially in districts where international demand is concentrated.

This is why timing matters. The political narrative is “introduce guardrails.” The market reaction can be “accelerate before guardrails bite.” That pre-implementation rush can temporarily inflate volumes and create false comfort in headline data. A strong print immediately before a legal tightening often reflects forward-pulled demand, not structural resilience.

Price Dynamics: Re-Acceleration, Then Uncertainty

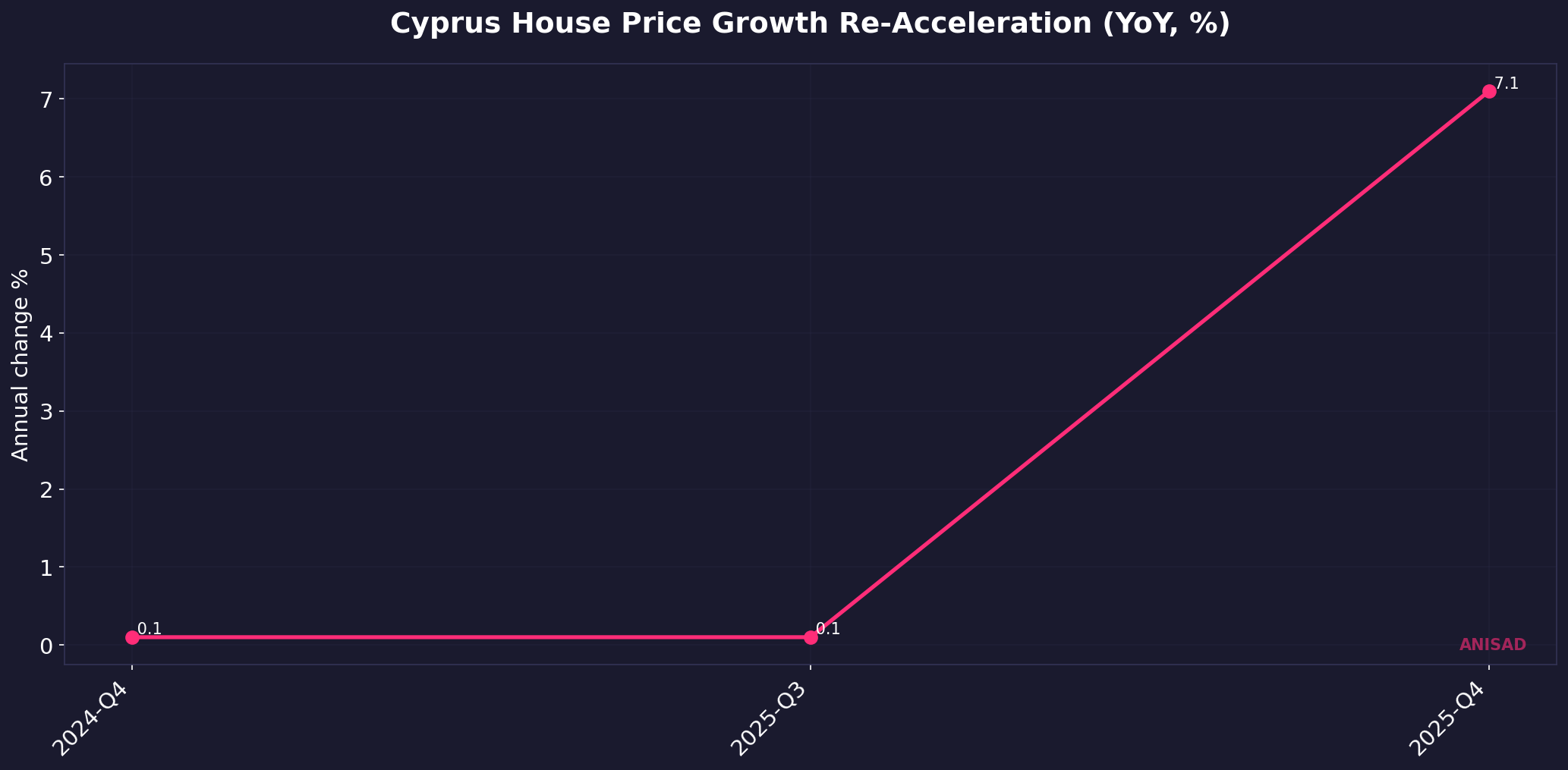

Price growth has already re-accelerated. Cyprus market tracking and related reporting show annual house-price growth moving back into high single digits by late 2025, with one widely cited Q4 reading at 7.1% YoY after a softer stretch earlier in the year. At the same time, foreign buyer sales growth in Q4 2025 was reported near +23.9% YoY, and non-EU share in January 2026 was reported around 30%. In simple terms: prices and foreign participation were rising together when the restriction agenda intensified.

That interaction creates a two-stage risk profile. Stage one: policy headlines can cool speculative bids in the most foreign-dependent pockets, especially where buyers expected unrestricted resale flexibility. Stage two: if domestic credit conditions remain supportive and supply stays tight, the adjustment may manifest more as transaction reshuffling than a broad price correction. In other words, headline price declines are possible, but not guaranteed. Liquidity distribution is the more probable battleground.

Who Wins, Who Loses

- Potential winners: domestic first-time buyers in submarkets where non-EU competition had become dominant.

- Potential winners: compliance-ready developers with transparent ownership structures and exposure to end-user demand.

- Potential winners: districts with balanced local + EU demand rather than one concentrated foreign segment.

- Potential losers: land-bank strategies reliant on quick foreign resale pipelines.

- Potential losers: intermediaries monetizing opaque nominee structures and low-disclosure vehicles.

- Potential losers: projects priced for uninterrupted non-EU absorption at premium velocity.

Importantly, “winner” does not mean immediate upside. If implementation is uneven or legal language stays ambiguous, all participants pay a temporary risk premium through slower closings and tougher due diligence. Clarity is the variable to watch: precise enforcement guidance can shorten the adjustment window; vague guidance can prolong it.

The Mediterranean Context: Cyprus Is Not Isolated

Cyprus is not acting in a vacuum. Across Mediterranean lifestyle markets, policymakers are testing how to limit social and strategic side effects of foreign demand without collapsing total transaction activity. Spain offers a useful contrast: non-resident foreign demand fell in 2025, yet total market activity remained robust due to resident and structural demand. The lesson for Cyprus is straightforward: policy can change buyer mix faster than it changes total demand. That is both an opportunity and a governance stress test.

If Cyprus executes this transition with predictable rules and fast administrative processing, it can reduce concentration risk while preserving investor credibility. If execution is fragmented, capital does not disappear—it reprices and reroutes. That rerouting may favor markets with fewer legal frictions, including peer Mediterranean jurisdictions competing for the same cross-border buyer base.

Forward Look: What To Track Over the Next 6–24 Months

- Implementation detail: final legal definitions, exemptions, and treatment of corporate beneficial ownership.

- Approval friction: time-to-approval and rejection rates for foreign-linked transactions after enactment.

- Composition shift: domestic vs EU vs non-EU shares by district, not only at national level.

- Liquidity stress: changes in days-on-market and discount-to-ask in foreign-heavy segments.

- Supply response: whether developers pivot product mix toward domestic affordability bands.

A policy shock can either improve market quality or freeze market confidence. The difference is implementation quality and predictability. Cyprus still has a realistic path to the former—but only if legal tightening is paired with administrative clarity and transparent enforcement.

Conclusion

The 2026 foreign-buyer restriction push is not a side story; it is now one of the central variables in Cyprus real estate pricing. The policy direction signals a deliberate shift from volume-at-any-cost toward controlled market structure. That can make the market healthier over time, but the transition will likely be uneven. For investors, the edge now comes less from broad market beta and more from regulatory literacy, district-level demand mapping, and execution discipline.

Data sources: Cyprus Mail coverage of foreign land purchase restriction bill (March 2026), Parliamentary/secondary reporting on non-EU buyer limits and strategic-zone constraints, Department of Lands and Surveys transaction reporting (January–February 2026), Cyprus Profile and StockWatch market summaries on HPI and foreign buyer growth (Q4 2025), CYSTAT and Eurostat house-price reference datasets (latest available quarters), Spanish Property Insight reporting on Spain foreign-demand composition (2025)