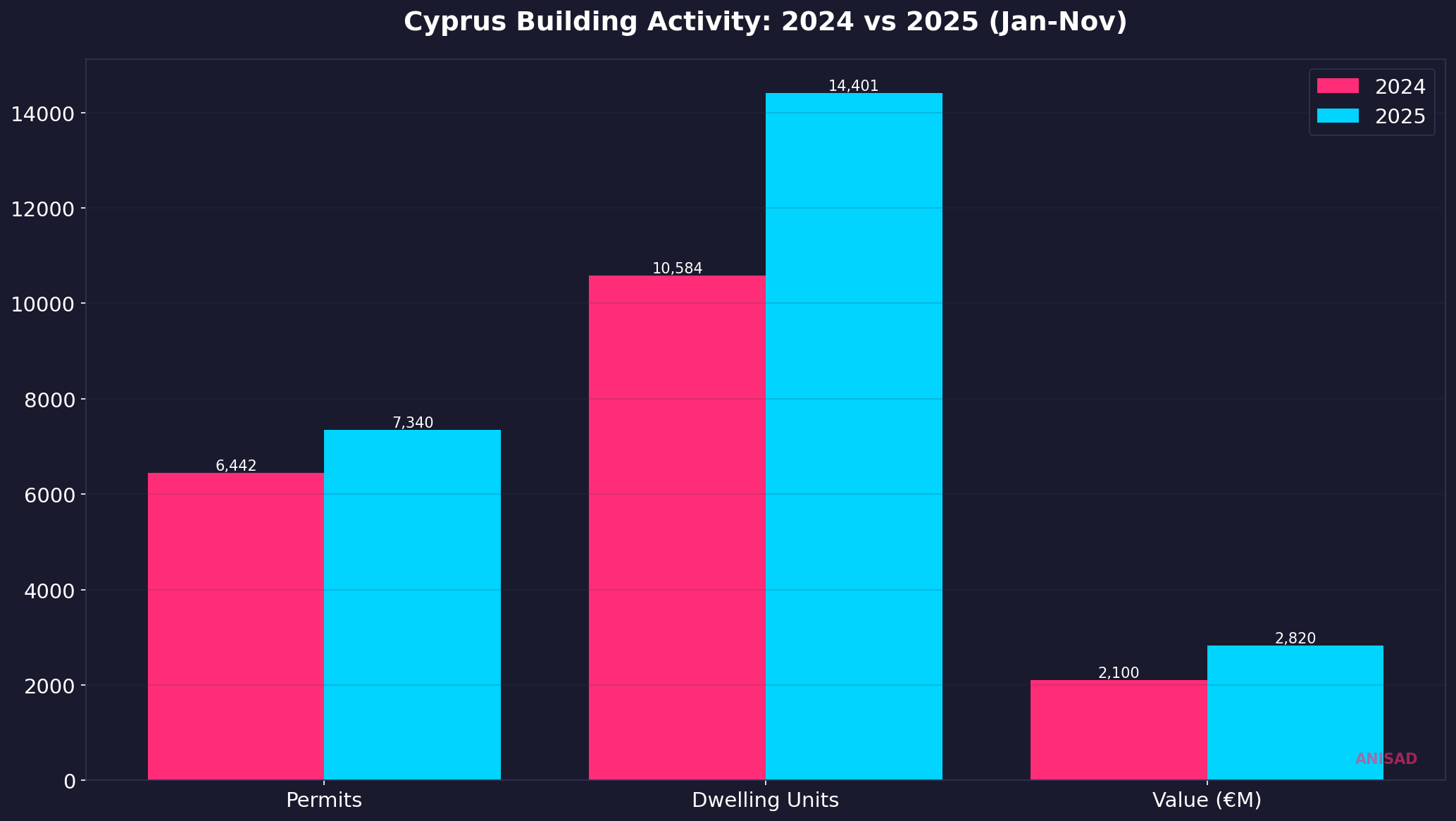

Cyprus is experiencing its most aggressive construction cycle in nearly two decades. With 14,401 dwelling units authorized in the first eleven months of 2025 alone — a 36% surge year-on-year and the highest figure since 2009 — the island is building at a pace that will reshape supply dynamics across every major city by 2028. But more supply does not automatically mean lower prices, and the risks embedded in this boom deserve as much attention as the headline numbers.

The Supply Wave in Numbers

CYSTAT data for January to November 2025 tells a clear story of acceleration. Building permits rose to 7,340, up 14% from 6,442 a year earlier. But the real signal is in dwelling units: the 14,401 authorized units represent a 36% increase over the 10,584 recorded in the same period of 2024. The total value of residential building permits reached €2.82 billion, a 32% jump, while total residential floor area expanded 35% to 2.18 million square meters.

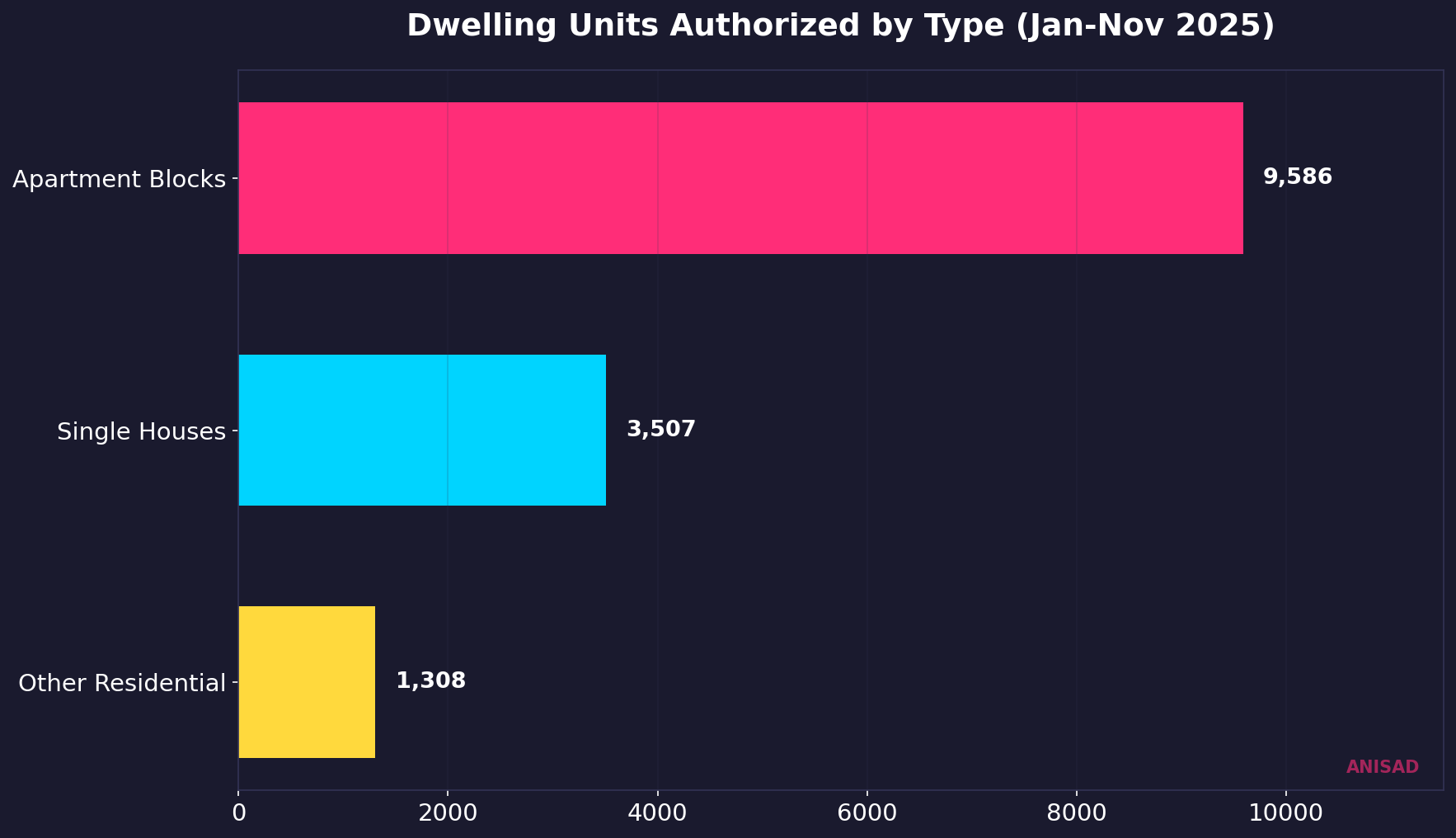

Apartment Blocks Dominate the Pipeline

The composition of new supply reveals a structural shift toward vertical development. Apartment blocks accounted for 9,586 authorized units in January-November 2025, up 43% from 6,654 a year earlier. Single houses also grew — reaching 3,507 units, a 35% increase from 2,593 — but apartments now represent roughly two-thirds of all new residential units. This reflects both developer economics (higher unit density, better margins per land plot) and buyer demand patterns: younger buyers and foreign purchasers increasingly prefer apartments over villas.

Government Adds Fuel: 2,500 Homes and a New Housing Fund

The supply wave is not purely market-driven. In March 2026, the Interior Minister announced a government construction drive targeting 2,500 new homes over two years, enabled by 46 planning incentive applications that unlock additional building coefficients. A new Affordable Housing Fund, capitalized at €12.5 millionfrom building coefficient purchases, will finance 400 affordable units through the Cyprus Land Development Corporation. A build-to-rent programme — rare in a country where owner-occupation exceeds 70% — signals a policy shift toward institutional rental models common in Western Europe.

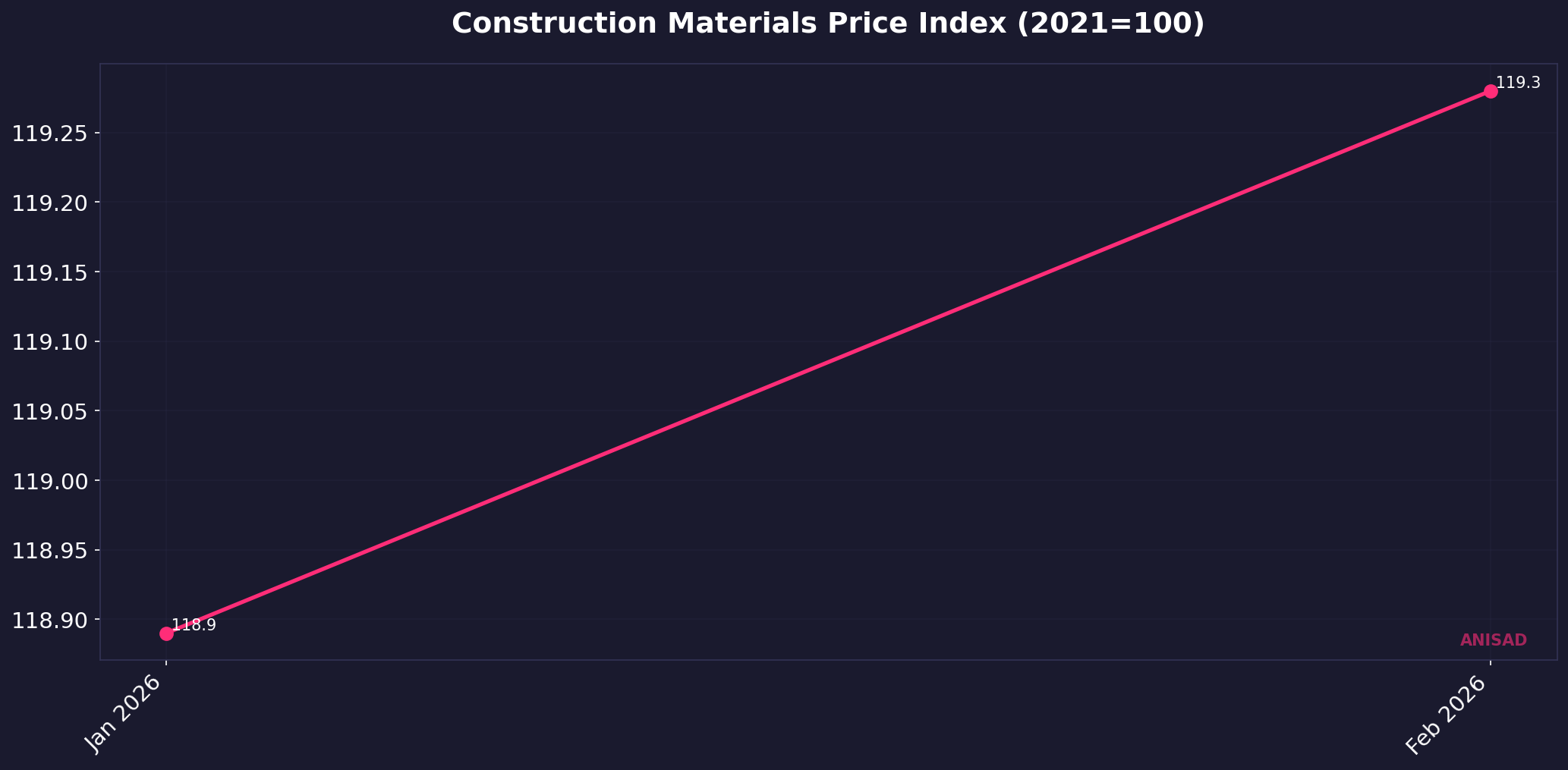

The Cost Squeeze: Materials and Delays

Supply is surging, but so are the frictions. The CYSTAT Construction Materials Price Index rose to 119.28 in February 2026 (base 2021=100), with electromechanical goods leading at +2.27% year-on-year. While the overall +0.60% increase appears manageable, geopolitical risk looms: the Iran conflict has disrupted Gulf shipping lanes, and industry analysts project a potential 15-20% surge in steel and aluminum prices through Q3 2026 if disruptions persist. This would directly compress margins on the thousands of apartment projects currently in the pipeline.

Meanwhile, the Property Developers Association has warned that permit processing times now exceed actual construction timelines in some cases. This bottleneck means that even permitted projects face unpredictable delays, creating a gap between authorized units and completed inventory.

Transaction Activity Confirms Demand — For Now

The demand side provides some reassurance. February 2026 saw 1,537 property transactions across Cyprus, an 11% increase year-on-year and just 44 below the February 2008 all-time record. Limassol led with 482 transactions (+24%), with domestic buyers up 26% and EU buyers surging 46%. But transaction data is a lagging indicator — it reflects properties already built and sold, not future absorption of the supply wave hitting the market in 2027-2028.

Who Wins, Who Loses

The construction supply wave creates clear winners and losers. Developers holding approved permitsbenefit from a market where demand still outpaces supply, especially if they locked in material contracts before potential war-related price spikes. First-time buyers stand to gain in the medium term as increased supply moderates price growth in the apartment segment. Construction firms benefit from a multi-year pipeline of work.

On the risk side, existing apartment owners in oversupplied areas may see appreciation slow as new inventory arrives. Small landlords face competition from institutional build-to-rent operators. And projects mid-construction with uncommitted material budgets are most exposed to geopolitical cost spikes.

What to Watch

The critical question is not whether supply is increasing — it clearly is — but whether demand can absorb it. Three metrics will determine the outcome: apartment absorption rates in Limassol and Nicosia (watch for rising time-on-market); construction material costs from March to June 2026 (the Iran conflict lag window); and the pace of government housing fund disbursements, which will signal whether the affordable housing programme is real policy or announcement theatre.

Cyprus is building again at a scale not seen since before the financial crisis. Whether this supply wave becomes a market correction catalyst or a sustainable expansion depends on what happens in the next 18 months.

Data sources: CYSTAT — Building Permits January-November 2025, CYSTAT — Construction Materials Price Index, January-February 2026, Department of Lands and Surveys (DLS) — Monthly Transaction Data, February 2026, Cyprus Mail — Residential building activity, March 2026, Cyprus Mail — Housing supply policy announcement, March 2026, Property Developers Association — Permit processing report, March 2026