Cyprus has opened one of the most consequential property-policy experiments in its recent history: legalise legacy planning breaches, accelerate title issuance, and tighten enforcement at the transfer stage. The state is effectively trading strict retrospective compliance for transactional finality. For investors and lenders, the key question is no longer whether irregular stock exists; it is how quickly that stock can be converted into legally transferable, financeable assets without eroding future compliance discipline.

What Changed in Practice

Three policy moves now sit in the same policy corridor. First, the Ministry of Interior's draft amendment framework would allow retroactive legalisation of unauthorised buildings that meet technical conditions, using a limited amnesty window and higher regularisation fees. Second, the cabinet approved title issuance mechanics for 7,859 refugee properties despite planning irregularities, with legal notations preserved. Third, the Department of Lands and Surveys activated administrative fine procedures under the Specific Performance regime, creating a direct enforcement lever when developers or vendors fail to complete deed transfer obligations.

Taken together, these actions shift Cyprus away from passive backlog management and toward active legal closure. The state is simultaneously widening the legalisation channel and hardening the transfer-compliance channel. That combination matters because title deed friction in Cyprus has historically been less about demand and more about legal-operational bottlenecks between planning, registry, and contracting.

Backlog Arithmetic: Why the Numbers Matter

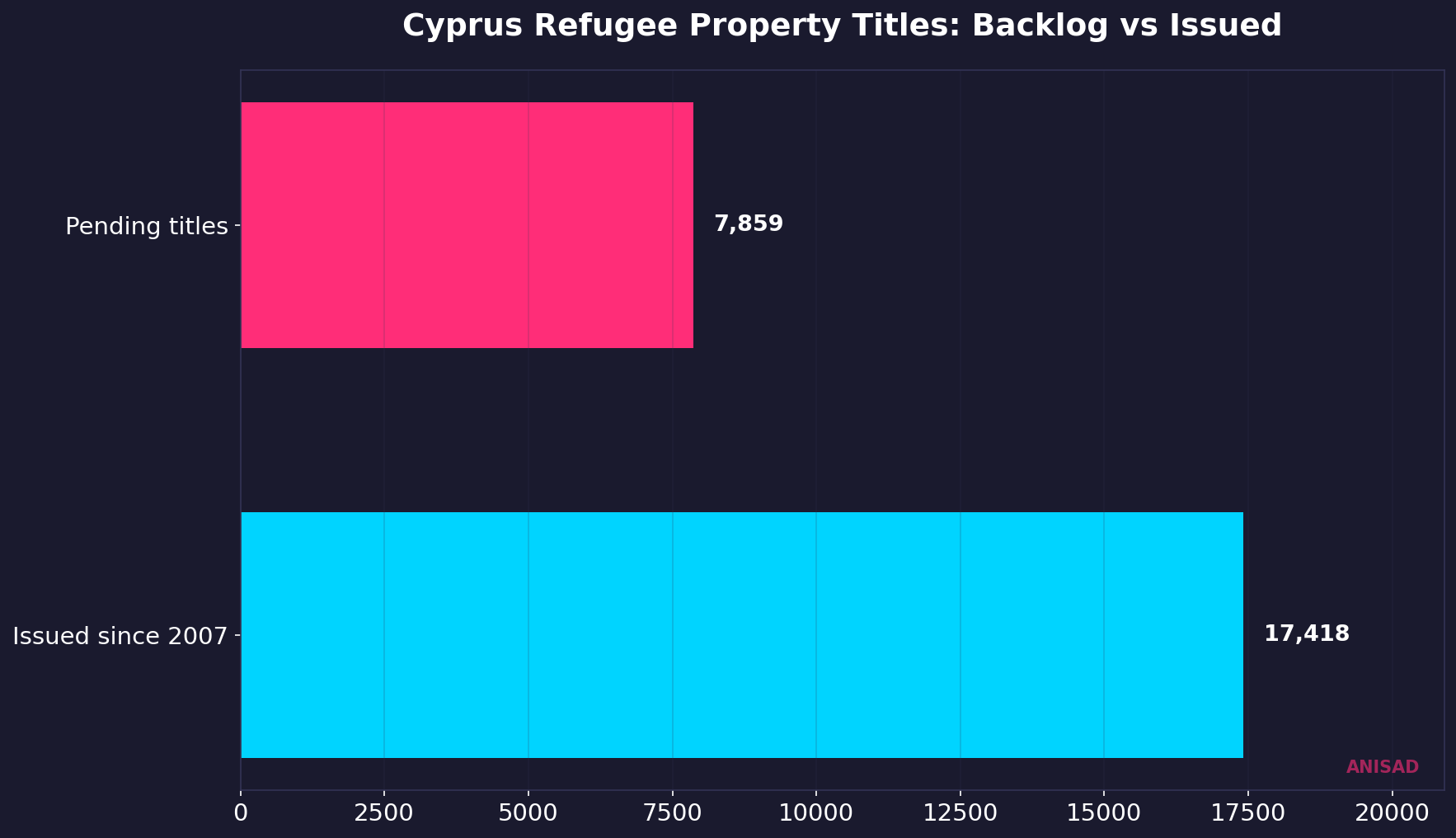

The published refugee-housing figures provide the clearest baseline for the scale of unresolved title conversion. Authorities report 7,859 pending titles and 17,418 already issued since 2007 in the same broader policy field. Even without overgeneralising beyond refugee stock, the ratio illustrates a central market reality: Cyprus still carries a meaningful inventory of legally constrained assets whose transactional utility depends on administrative normalisation rather than new construction cycles.

For banks, this is collateral quality policy disguised as social-administrative reform. As more units become title-eligible, collateral enforceability improves, refinancing pathways expand, and intergenerational transfer friction declines. For buyers, clearer deed pathways compress legal uncertainty premiums that would otherwise be priced into resale negotiations.

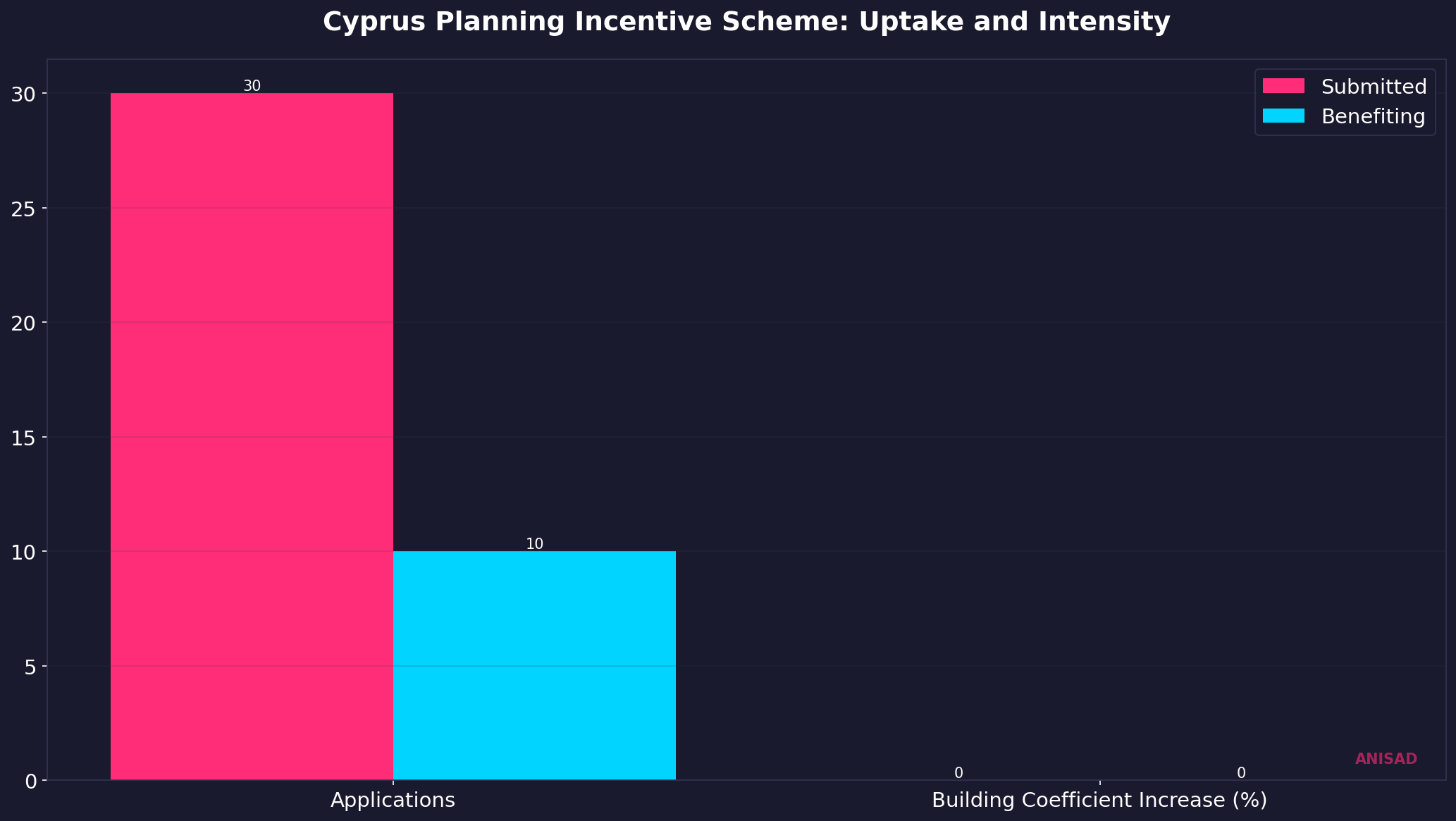

Planning Incentives as a Second-Layer Tool

In parallel, the cabinet extended the education-sector urban incentives framework through 2027, reporting 30 applications in year one, with 10 already positioned to benefit from the scheme and permitted building-coefficient uplifts of 10-25% depending on area. This is not a marginal zoning tweak. It is a capacity-allocation instrument that links planning flexibility to public-interest outputs and, in this case, to affordable housing financing channels.

From a market-structure perspective, this creates a policy stack: regularise old non-compliance, enforce transfer discipline on current stock, and calibrate future build intensity through targeted incentives. If executed coherently, this can improve both market liquidity and medium-term supply elasticity. If executed unevenly, it can institutionalise expectations of future exceptions.

Who Gains, Who Carries New Risk

- Legacy owners in irregular stock gain a path to legal transferability and cleaner exit options.

- End-buyers gain from improved deed certainty, but must still price location-specific planning risk.

- Banks gain higher-quality collateral pools if title conversion actually completes at scale.

- Compliant developers risk competitive distortion if repeated amnesties reduce the penalty for non-compliance.

- Municipal planning systems face execution risk: throughput must increase without lowering technical scrutiny.

The Core Policy Trade-Off

Cyprus is pursuing a dual narrative: pragmatic market repair and institutional deterrence. The repair argument is strong: unresolved title structures are economically costly and socially corrosive. The deterrence argument is harder: if actors believe non-compliance will eventually be regularised at manageable cost, enforcement credibility weakens over time. The decisive variable is not the amnesty text itself; it is post-amnesty behaviour. Specifically, whether fine mechanisms, transfer controls, and planning audits remain consistently active after the backlog clears.

An amnesty can be a one-time market reset. Repeated amnesties become a pricing signal that compliance is optional.

12-24 Month Outlook

- Transaction quality should improve first in segments where title resolution can be processed quickly.

- Mortgage underwriting may gradually re-rate previously discounted assets once legal documentation stabilises.

- Developer behaviour will hinge on enforcement consistency during new permitting cycles, not on past regularisation rhetoric.

- Policy credibility will be tested by whether administrative fines are visible, predictable, and legally durable.

- If implementation velocity lags, the market may see temporary legalisation optimism without full liquidity conversion.

Bottom Line for Investors and Operators

This is not a cosmetic policy episode. It is a structural attempt to convert legal ambiguity into tradable certainty while preserving forward discipline. Investors should treat 2026-2027 as an implementation cycle and monitor three indicators: title conversion throughput, enforceability of transfer penalties, and evidence of planning compliance in newly initiated projects. If those indicators move together, Cyprus improves market depth without sacrificing legal integrity. If they diverge, moral hazard will be repriced into land, development, and financing decisions.

Data sources: Cyprus Ministry of Interior draft consultation on Roads and Buildings Regulation Amendment No.2/2026, Cyprus Cabinet decision on refugee-property title issuance (April 2026), Department of Lands and Surveys notice on administrative fines under Specific Performance Law 81(I)/2011, Cabinet extension briefing on education-sector urban incentives and affordable-housing linkage